Introduction

Finance is one of the most important parts of modern life. It allows people, businesses, and governments to move money, invest, and plan for the future. Over time, technology has deeply changed how finance operates. One of the biggest changes in recent years is the rise of decentralized finance, also known as DeFi.

Traditional finance has long been the foundation of global money management. People depend on banks, insurance firms, and stock exchanges to handle their funds. These institutions act as middlemen between users, ensuring safety and regulation. In contrast, decentralized finance aims to give people direct control over their money.

The growing interest in decentralized finance has created discussion about whether it can replace traditional systems. Some believe DeFi offers more freedom and fairness by removing intermediaries. Others argue that banks and established platforms still provide much-needed security and trust. Understanding both sides helps to see how finance might evolve in the future.

The comparison between decentralized finance and traditional finance highlights a shift in how trust, control, and access are managed. Both systems aim to deliver financial services, but they follow very different operating models. Understanding these differences is important for evaluating future financial systems.

Key Takeaways

- DeFi total value locked reached USD 247 billion in Q2 2025, marking 31% year-on-year growth and confirming renewed momentum across decentralized finance markets.

- Around 5.4 billion people worldwide remain unbanked or underbanked, with DeFi platforms increasingly serving as an alternative access point to financial services.

- The five largest U.S. banks together hold about USD 19.7 trillion in assets, highlighting the scale gap between traditional banking and decentralized finance.

- Preference for decentralized platforms is rising among younger users, with 57% of Millennials and Gen Z favoring DeFi apps over mobile banking in 2025.

DeFi Lending Landscape

- Aave V2 led the market with USD 4.1 billion in lending volume, positioning it as the top DeFi lending platform.

- JustLend followed with USD 3.39 billion in lending activity, ranking second among major protocols.

- Venus recorded USD 878.25 million in lending volume, securing third position.

Efficiency and Operational Metrics

- Traditional finance continues to process far larger transaction volumes, handling around USD 405 trillion per quarter, compared with USD 1.9 trillion for DeFi.

- Despite lower volumes, DeFi delivers much faster execution, particularly for payments and lending activities.

- Cross-border transfers in traditional finance take about 28 hours on average and cost roughly USD 14.7 per transaction.

- DeFi transfers on Layer-2 networks settle in about 3.6 seconds, with a median fee of just USD 0.06.

- Loan approval timelines show the widest gap, with traditional finance taking 1–3 days, while DeFi loans execute in an average of 0.08 seconds through smart contracts.

User Metrics and Interest Rates

- Active DeFi users reached 312 million globally in Q2 2025, while the number of traditional bank account holders continues to grow at 6.9% annually.

- DeFi platforms offer higher yield potential, averaging 8.2% across staking and lending, compared with a global average savings rate of 2.1%.

- Fraud and security risks remain on both sides, with USD 2.8 billion in U.S. fraud losses reported in traditional finance during H1 2025, versus USD 1.1 billion lost to DeFi protocol hacks.

- Trust perceptions differ sharply, as only 19% of traditional finance customers feel banks act in their best interest, while 63% of DeFi users report higher satisfaction due to transparency and on-chain visibility.

Market Size and Growth

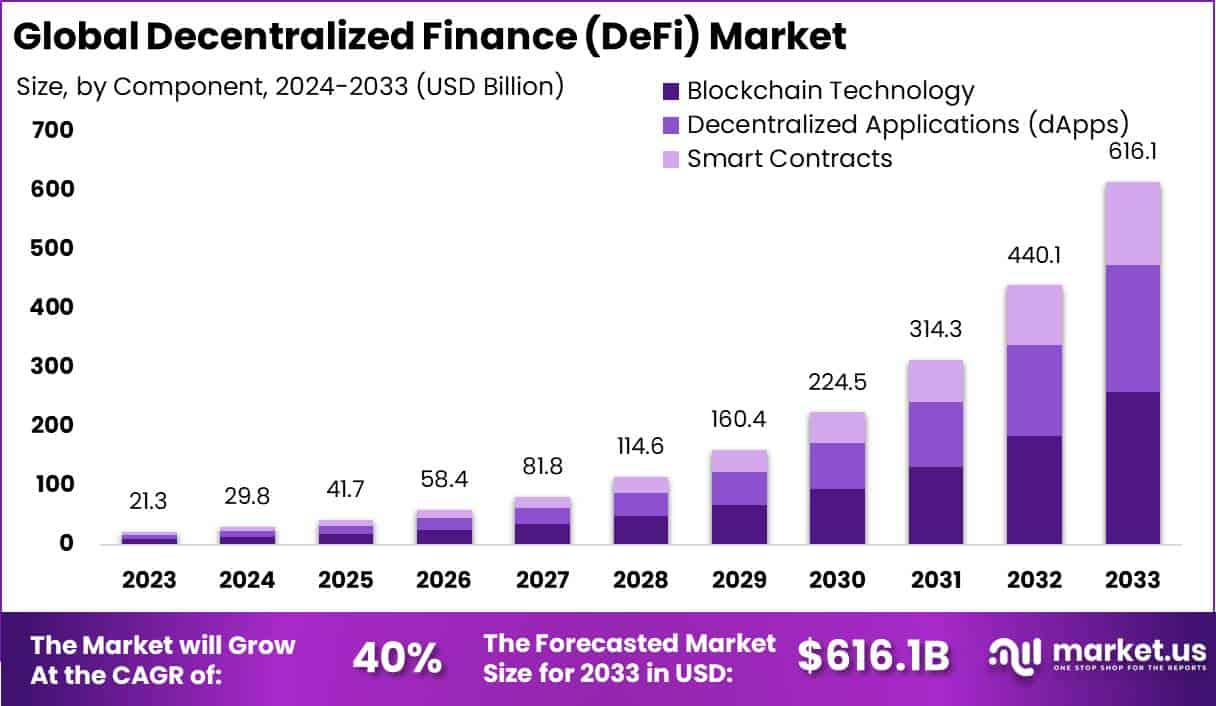

- The global Decentralized Finance (DeFi) market is projected to reach approximately USD 616.1 Billion by 2033, rising from USD 21.3 Billion in 2023. This growth reflects a strong CAGR of 40% during the forecast period from 2024 to 2033. Rapid adoption of blockchain-based financial services and decentralized platforms continues to support market expansion.

- In 2023, North America held a dominant position with more than 36% market share, generating around USD 7.6 Billion in revenue. The region benefits from early adoption of digital assets, strong developer activity, and advanced financial infrastructure. Ongoing innovation and regulatory clarity continue to support DeFi adoption across the region.

- DeFi platforms process around USD 1.9 trillion in transactions per quarter and generate roughly USD 32 billion in annual revenue.

- The global fintech market reached USD 1.5 trillion in 2025, with DeFi contributing close to 16% of total value.

- Traditional banks still control 72% of consumer lending, while DeFi accounts for 6.8%, indicating early but growing penetration.

- Layer-2 DeFi ecosystems generated about USD 13 billion in gas fees, reflecting rising on-chain activity.

- User funds in DeFi have grown by 3.5x since 2023, underscoring accelerating adoption and capital inflows.

(image credit – market.us)

Geographic Distribution

- Asia accounts for 33% of global DeFi users in 2025, with Vietnam, India, and the Philippines among the strongest adoption markets.

- Latin America represents 21% of DeFi usage, led by Brazil, Argentina, and Colombia, where currency volatility and limited banking access support adoption.

- Sub-Saharan Africa holds 19% of active DeFi users, particularly in Nigeria and Kenya, where mobile-first financial behavior is widespread.

- North America and Europe together host 47% of the world’s banked population, yet contribute only 14% of global DeFi adoption.

- About 78% of traditional banking institutions in emerging markets still require in-person identity verification, limiting digital reach.

- DeFi accessibility continues to widen, with 86 countries now supporting fiat on-ramps into decentralized platforms.

- In the U.S., 12% of households used at least one DeFi application in 2025, indicating early but growing mainstream penetration.

- Mobile-first regions dominate new adoption, with 53% of wallet creations in 2025 originating from Southeast Asia and Africa.

- The Middle East and North Africa contributed 16.4% of global DeFi adoption growth in 2025, reflecting expanding regional interest.

- Traditional banking infrastructure remains highly concentrated, with 91% of investment directed toward G20 countries.

(data source: coinlaw.io)

Use Case of DeFi

| Use Case | Description |

|---|---|

| Lending and Borrowing | Users lend or borrow digital assets through smart contracts by depositing crypto as collateral, without bank approval or credit checks. Lenders earn interest from liquidity pools, while borrowers access funds quickly. Platforms such as Aave and Compound enable open access to these services. |

| Decentralized Exchanges (DEXs) | Users trade cryptocurrencies directly using automated market makers instead of centralized exchanges. This enables instant token swaps with lower fees and full asset control. Transactions settle on blockchains for transparency. |

| Stablecoins | Digital tokens pegged to stable assets like the US dollar reduce price volatility. They are used for payments, savings, and trading across DeFi platforms. Stablecoins link traditional money with digital finance. |

| Prediction Markets | Users place bets on real-world events such as elections or sports outcomes. Collective forecasts are created without centralized bookmakers. Smart contracts automatically manage payouts. |

| Synthetic Assets | Blockchain tools provide exposure to assets like stocks or commodities without physical ownership. Crypto collateral backs these instruments, removing the need for custodians. This offers new investment alternatives. |

Benefits

| Benefit | Explanation |

|---|---|

| Accessibility | Anyone with internet access and a digital wallet can use DeFi services. No bank accounts or credit scores are required. This supports financial inclusion, especially in underserved regions. |

| Lower Costs | Removing intermediaries reduces transaction and service fees. Users benefit from better interest rates and lower processing costs. Blockchain automation improves efficiency. |

| Transparency | All transactions are recorded on public blockchains for real-time verification. This reduces fraud and increases trust. Smart contracts enforce rules automatically. |

| Speed and Availability | DeFi operates around the clock with fast settlement times. Cross-border payments occur instantly. No approval delays exist. |

| User Control | Users maintain custody of their funds through personal wallets. Programmable finance tools provide flexibility and independence. Financial decisions remain fully user controlled. |

Limitations of DeFi

| Limitation | Details |

|---|---|

| Security Risks | Smart contract vulnerabilities and hacks can result in financial losses. Unlike banks, DeFi platforms usually lack insurance protection. Users are responsible for securing their assets. |

| Complexity | Wallet management and blockchain processes can be confusing for new users. Errors and scams are more likely without proper knowledge. Limited support increases user risk. |

| Regulatory Uncertainty | Unclear regulations create legal and tax risks. Lack of oversight may slow adoption and increase fraud exposure. Consumer protections remain limited. |

| Scalability Issues | Network congestion can raise fees and slow transactions. Current throughput limits restrict mass adoption. Platform interoperability challenges persist. |

| Lack of Consumer Protections | No formal dispute resolution or refunds exist. Asset price volatility increases financial risk. Governance structures may still concentrate power. |

Recent Developments

- World Liberty Financial raised $550 million in its token sale, ranking second among 2025’s largest DeFi launches; a December spending proposal split community opinions with 80% of tokens still locked.

- April 2025: Ethereum implemented the Dencun upgrade, improving Layer-2 throughput by 3.7x while reducing transaction costs and network congestion.

Explore More

- Top Drone Companies Shaping Global Market Growth

- Statistical Analysis of the Insurance Industry

- Open Banking vs Open Finance

- Embedded Lending vs Embedded Finance

- Digital Assets vs Cryptocurrency: Key Insights

- A New Financial Era: Comparing DeFi and Traditional Finance

The Future of Finance

The future of finance will likely involve both systems working together. Traditional finance provides structure, legal support, and trust. DeFi brings innovation, accessibility, and efficiency through technology. A blend of both could create a more balanced and dynamic financial world. Many banks and institutions are already exploring blockchain solutions.

They see the value in combining transparency and technology with their existing trust networks. Such cooperation may lead to faster and more secure global transactions. It could also help governments manage digital currencies safely. Public perception will shape how this future develops. People want convenience but also need protection. For finance to evolve successfully, innovation and regulation must grow side by side. The future will rely on finding harmony between freedom and responsibility.

Conclusion

Traditional finance provides stability, legal protection, and institutional trust. It is well suited for users who value security and structured oversight. However, access and efficiency remain challenges in some regions. Decentralized finance offers open access, transparency, and operational efficiency. It empowers users with direct control but increases individual responsibility and risk. Technical understanding is essential for safe participation. Both systems serve different needs and user preferences. Rather than replacing one another, they may continue to evolve side by side. Future financial systems may combine elements of both models.

Sources

- https://www.calibraint.com/blog/top-defi-use-cases-and-applications

- https://www.debutinfotech.com/blog/top-defi-use-cases

- https://www.linkedin.com/pulse/top-11-decentralized-finance-development-use-cases-2025-2sxee/

- https://www.techaheadcorp.com/blog/decentralized-finance-for-enterprises/

- https://entethalliance.org/specs/defi-risks/

- https://www.geeksforgeeks.org/blogs/top-challenges-faced-by-defi-dapp-solutions/

- https://www.tencentcloud.com/techpedia/101086

- https://market.us/report/decentralized-finance-defi-market/

- https://coinlaw.io/defi-vs-traditional-banking-statistics/

- https://www.fisdom.com/decentralized-finance-defi/

- https://www.tencentcloud.com/techpedia/101086

- https://www.telco.in/en/support-center/cryptocurrency-basics/how-defi-differs-from-traditional-finance