Embedded Finance Statistics: Embedded finance is changing how financial services are offered by seamlessly integrating payments, lending, insurance, and investments into non-financial platforms like apps and websites. This trend is making financial products more accessible, user-friendly, and affordable, without customers needing to leave the platforms they already use daily. Its rapid growth is reshaping commerce and banking, driven by rising digitalization and demands for faster, personalized financial experiences.

Embedded finance refers to embedding financial services such as payments, credit, insurance, or investment options directly into non-financial digital platforms. Instead of going to a bank, customers can access these services directly within apps for shopping, messaging, or other services. This dramatically lowers the barriers for businesses to offer financial features and enhances customer convenience by keeping everything in one place.

Editor’s Choice – TLDR

- The projected value of embedded finance transactions is expected to reach USD 7 trillion by 2026.

- More than 70% of logistics payment facilitators plan to roll out embedded finance within the next five years.

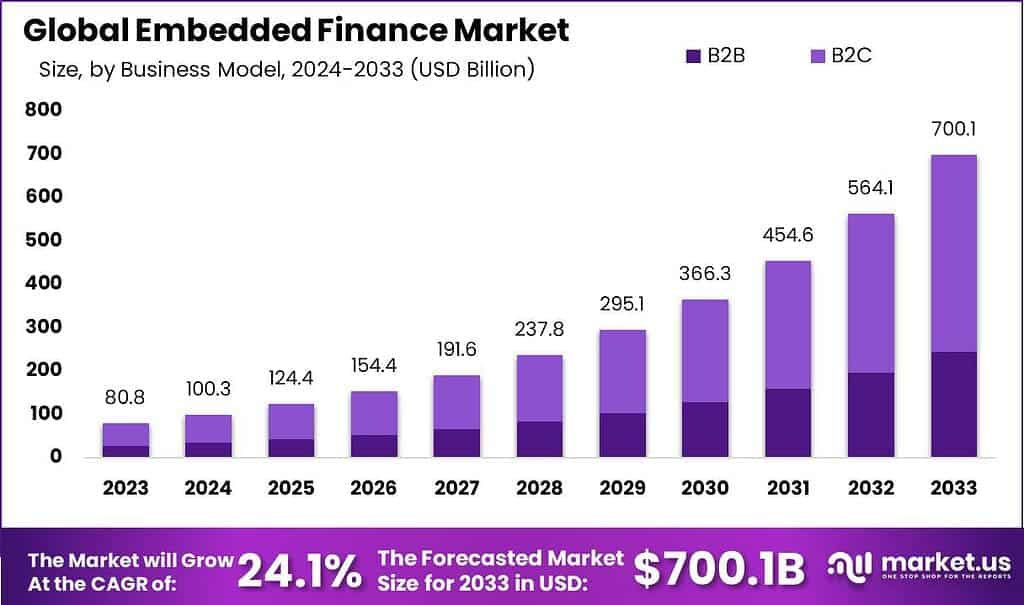

- According to Market.us, The Global Embedded Finance Market is projected to reach USD 700.1 billion by 2033, rising from USD 80.85 billion in 2023 at a 24.10% CAGR.

- North America held over 35% share in 2023, with revenue of USD 28.3 billion.

- Sponsor banks report that 51% of their total revenue and deposits come from embedded finance partnerships.

- 67% of consumers use embedded payment solutions in their daily transactions.

- 64% of businesses plan to introduce embedded finance solutions in 2025.

- 20 to 25% of lending revenue is expected to come from embedded finance by 2030.

- AI-driven systems can detect fraud by up to 50%, improving risk management and platform security.

- Embedded financial services placed inside e-commerce and software platforms processed USD 2.6 trillion in 2021, equal to roughly 5% of all US financial transactions, and are projected to surpass USD 7 trillion by 2026.

- 45% of Gen Z and Millennials used BNPL services in the past year.

- Over 70% of logistics and wholesale trade platforms are expanding embedded finance products, reflecting strong industry-wide adoption.

Adoption and Business Impact

- 64% of businesses plan to launch embedded finance solutions in 2025 to enhance customer experience and strengthen revenue generation.

- Companies adopting embedded finance report 2 to 5 times higher customer lifetime value, supported by stronger engagement and better retention.

- Customer acquisition costs decline by around 30% when embedded financial services are integrated into existing digital journeys.

- Enterprise businesses can generate up to USD 70 in additional annual revenue per customer from transaction fees and improved retention rates.

- Traditional banks are shifting toward partnership models by collaborating with fintech providers to deliver embedded financial services and maintain competitive relevance.

You May Also Like to Read

- Digital Banking Statistics

- Creator Economy Statistics

- Cybersecurity Statistics

- EdTech Statistics

- Podcast Statistics

- eSports Statistics

- DeepSeek Statistics

Embedded Finance Market Size

- In 2023, the Embedded Payment segment led the embedded finance market with over 47% share, supported by strong adoption in e-commerce and digital platforms.

- The Business-to-Consumer (B2C) segment held a dominant position in 2023, capturing more than 65% share, driven by consumer demand for integrated financial services.

- The Retail sector was the leading industry segment in 2023, accounting for over 34% share, reflecting rising use of embedded payments, lending, and checkout financing.

- North America remained the dominant regional market in 2023 with more than 35% share, reaching around USD 28.3 billion in revenue due to strong fintech ecosystems and high digital adoption.

(Source: Market.us)

Regional Insights

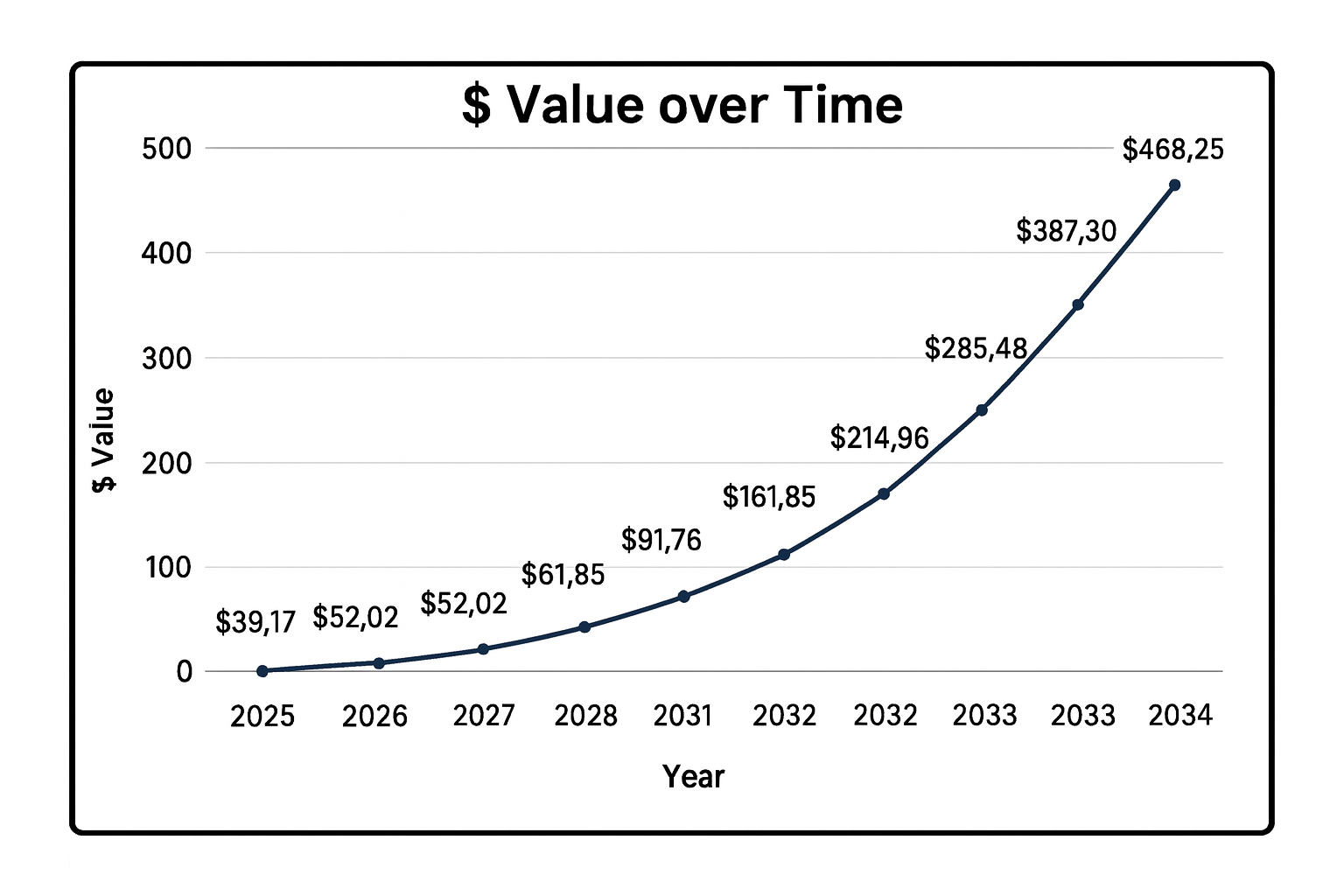

The U.S. embedded finance market surpassed USD 39.17 billion in 2025 and is expected to reach nearly USD 468.25 billion by 2034, advancing at a strong CAGR of 31.85% during 2025–2034.

This growth is being supported by rising demand for integrated financial services within retail, e-commerce, mobility, and software platforms.

| Year | Value (USD) |

|---|---|

| 2025 | $39.17 |

| 2026 | $52.02 |

| 2027 | $69.09 |

| 2028 | $91.76 |

| 2029 | $121.87 |

| 2030 | $161.85 |

| 2031 | $214.96 |

| 2032 | $285.48 |

| 2033 | $387.30 |

| 2034 | $468.25 |

North America has contributed more than 33% of revenue share in 2024.

(Source: precedence research)

Embedded Lending Market Size

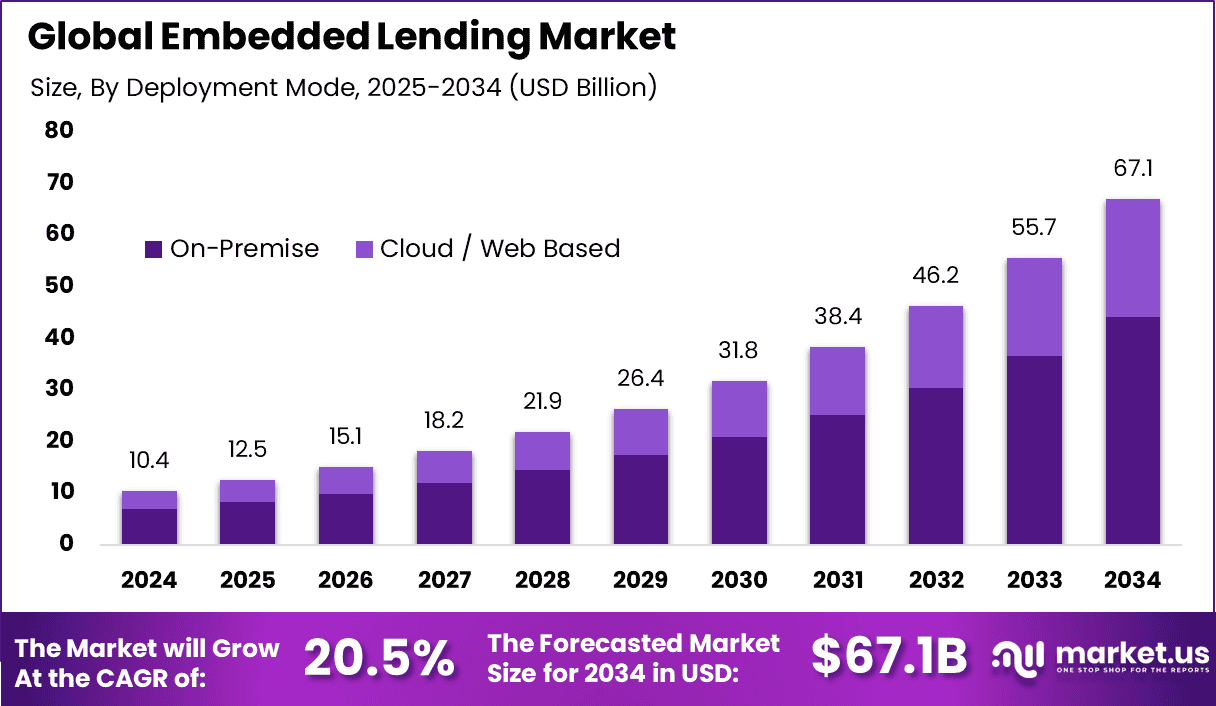

- In 2024, the embedded lending platform segment led the solution category with a 68.4% share.

- The on premise deployment model maintained leadership with 65.7% of the market.

- Large enterprises were the strongest adopters, holding a 72.3% share in 2024.

- The retail industry was the top vertical, accounting for 35.7% of total demand.

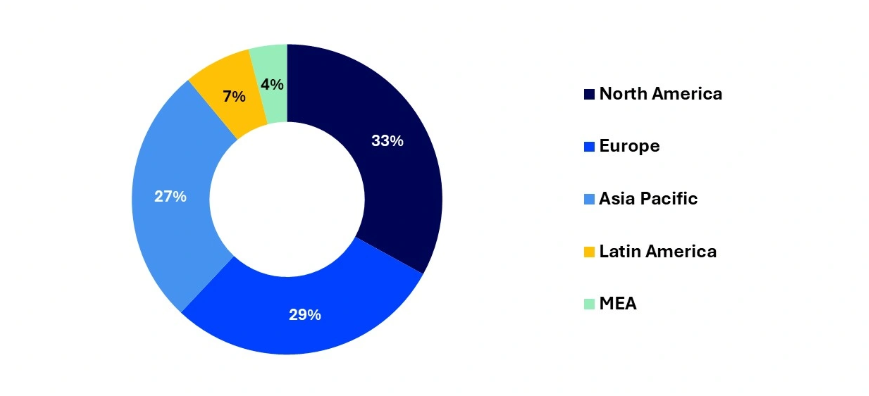

- North America captured 37.4% of the global market.

- The US market reached USD 3.32 Billion in 2024, supported by a 16.5% CAGR.

- More than 40% of consumers are willing to switch to a platform that offers embedded lending.

- 56% of Gen Z and 55% of millennials express high interest in using embedded lending services.

- Around 29% of consumers would use embedded lending for unexpected emergency expenses.

- US embedded finance revenue is projected to rise from USD 30.82 Billion in 2024 to USD 89.59 Billion by 2029, reflecting strong long-term adoption.

- 96% of sponsor banks maintain multiple embedded finance partnerships, often managing 6 to 10 active collaborations.

- Growth is supported by advances in APIs, payment infrastructure, and strategic partnerships across ecosystem players.

- Embedded financial delivery models improve customer experience by combining financial and non-financial services, though application friction remains a barrier in some markets.

(source: market.us)

Recent Developments

- March 2025, Walmart partnered with JPMorgan to roll out embedded banking for marketplace merchants on Walmart’s platform, giving sellers real‑time payouts and digital accounts inside the commerce environment rather than through a separate bank relationship, which tightens cash‑flow control for small businesses.

- February 2025, Affirm entered a strategic partnership with FIS to embed buy now, pay later plans into FIS‑issued debit cards, so banks can switch on installment options directly inside their digital banking apps and keep customers within their own channels instead of losing those transactions to standalone BNPL providers.

- January 2025, Green Dot expanded its embedded finance offering by deepening its Banking‑as‑a‑Service support for Dayforce Wallet, allowing employers to give workers on‑demand access to earned wages through a mobile app, linked prepaid cards, and fee‑free ATM withdrawals, positioning embedded payroll wallets as a core use case in workforce management.

- Q1 2025, Apple introduced an embedded credit line within Apple Pay in early 2025, using Green Dot’s BaaS stack to underwrite and service financing behind the scenes so eligible users can access revolving credit from within their existing wallet experience.

Key Trends and Beyond

- AI for Risk Assessment: Financial institutions are using AI to assess creditworthiness and detect fraud with high accuracy. These systems are helping reduce default rates by 20% to 30%.

- B2B BNPL Expansion: The Buy Now Pay Later model is moving into the business-to-business market. B2B BNPL transactions are projected to reach USD 687 billion by 2028.

- Embedded Insurance Growth: Adoption of embedded insurance is increasing. 81% of firms in North America consider it a strategic requirement for improving customer retention.

- ESG Integration: Platforms are adding sustainable finance features such as green investment products and ESG scoring to meet rising demand for responsible financial management.

- Regulatory Shifts: Global regulatory frameworks for open banking and data privacy are expanding, shaping how financial data is stored, accessed, and processed.

Benefits of Embedded Finance

Benefits for Businesses

- New revenue streams: Firms can earn from interchange and transaction fees, lending margins, insurance commissions, and value‑added subscriptions layered on top of financial features.

In some surveys, more than 70% of mid‑market platforms say embedded finance has already lifted their per‑customer revenue or ARPU. - Higher customer retention: When users can pay, finance purchases, or manage balances inside one app, session length and repeat usage rise, and churn drops.

Platforms that add wallets, cards, or lending often see double‑digit gains in engagement, because customers have fewer reasons to leave for a bank or rival service. - Competitive differentiation: SaaS, e‑commerce, and marketplaces use embedded finance to stand out with sector‑specific accounts, cards, or credit (for example, tools tuned to small merchants, drivers, or freelancers). Analysts now view embedded finance as a core strategy, not an add‑on, in a market expected to exceed USD 1.7 trillion by 2034, so early movers can lock in share and data advantages.

Benefits for Consumers

- Frictionless transactions: One‑click or in‑app payments remove the need to type card details or open a separate banking app, cutting checkout abandonment.

In some demographics, more than 80% of younger users prefer digital or in‑app payments over traditional card entry because of speed and ease. - Greater financial accessibility: Embedded lending and BNPL give instant decisions at checkout, often for users who may not have traditional credit lines, widening access to short‑term finance. In markets like India and Southeast Asia, embedded credit inside super‑apps and marketplaces is becoming a primary on‑ramp to formal finance for small merchants and gig workers.

- Convenience and speed: Users can see balances, repay installments, buy insurance, or invest small amounts without leaving their main app, trimming process time from days to minutes. This integrated experience is a major reason embedded finance is growing at a CAGR above 30%, as customers increasingly expect banking‑like features wherever they already shop or work.

Opportunities in embedded finance

- Vertical SaaS and Platforms: The biggest opportunity sits inside software used every day by SMEs, like tools for retail, logistics, healthcare, creators, or restaurants. These platforms can layer in accounts, cards, payouts, and working‑capital lending that match the workflows of their niche, turning from “tools” into full business operating systems.

- B2B Marketplaces and Supply Chains: Online B2B marketplaces and procurement platforms can embed invoice financing, pay‑later for buyers, and early‑payment discounts for suppliers. This solves a real pain point: working capital. Whoever controls these flows can earn from interest, fees, and higher retention while making the platform the default place to trade.

- Embedded Credit for Under‑served Segments: Large opportunities lie in credit for small merchants, gig workers, and first‑time borrowers who are invisible to traditional banks. Platforms already see their orders, earnings, and repayments, so they can underwrite smarter, offer smaller tickets, and price risk better than a bank that only sees a static statement.

- Super‑apps and Everyday Consumer Journeys: Consumer apps in mobility, food delivery, travel, gaming, and social commerce can keep users inside their ecosystem with wallets, loyalty cards, micro‑insurance, and savings pockets. The opportunity here is not just fee income but owning the entire daily money journey so competitors never even see the customer.

- Data, AI, and Risk Infrastructure: Another deep opportunity is on the “picks and shovels” side: providing APIs for KYC, fraud detection, credit scoring, and compliance that make embedded finance safe. As more non‑financial brands enter the space, they will pay specialists to handle risk, scoring, and real‑time decisioning in the background.

- Banks and Licensed Financial Institutions: For banks, the opportunity lies in becoming the regulated engine behind many of these experiences. Instead of fighting platforms, they can power dozens of them with accounts, lending lines, and compliance, earning steady wholesale revenue while platforms handle UX and distribution.

- New Revenue Models for Non‑Financial Brands: Any brand with a loyal audience can explore co‑branded cards, subscription bundles that include financial benefits, or embedded protection (for example, extended warranty, device cover, ticket protection). Done well, this turns a one‑time product sale into a long‑term relationship with recurring income.

Key Examples of Embedded Finance

Embedded finance shines through real-world cases where companies weave payments, loans, insurance, and more right into their apps or sites, keeping users hooked without extra hassle. These examples show how everyday platforms turn into one-stop financial hubs, boosting sales and loyalty along the way. From ride-sharing to online stores, the shift feels natural and smart.

- Embedded Payments: Digital wallets like Apple Pay and Google Pay let users tap to pay in apps from Uber rides to coffee orders, skipping card details every time. Uber’s in-app payments handle fares instantly, pulling from linked accounts for seamless trips. This setup cuts checkout friction and speeds up transactions everywhere from stores to services.

- Embedded Lending: Buy Now, Pay Later options from Klarna and Affirm split big purchases into easy chunks at checkout on sites like Amazon or Walmart. Shoppers pick installments without credit checks dragging things out, helping more buys go through. DoorDash even lends cash advances to restaurants based on their sales, paid back as business flows.

- Embedded Banking: Platforms like Shopify Balance give merchants bank accounts, payments, and cash tools all in one dashboard, ditching traditional banks. Stripe Treasury does the same for apps, handling deposits and transfers without leaving the platform. Freelance site Malt pays workers upfront via partners, settling later with clients for quicker cash flow.

- Embedded Insurance: Booking sites like Booking.com offer travel coverage right at checkout, covering trips without extra sites or forms. Tesla bundles car insurance into vehicle buys, using driving data for custom rates on the spot. This on-demand protection fits perfectly with purchases, adding peace of mind instantly.

- Embedded Investing: Apps such as Robinhood and Revolut let users trade stocks or crypto with a few taps, no separate broker needed. Cash App adds micro-investments from spare change, growing savings effortlessly. These tools pull people into investing by keeping it simple and tied to daily apps.

Conclusion

Embedded finance has reshaped how businesses deliver value in 2025, embedding payments, lending, and insurance directly into everyday platforms like e-commerce sites and gig apps. This shift boosts user stickiness and opens fresh revenue streams without forcing customers to jump between apps, all powered by robust APIs and open banking frameworks.

Looking ahead, AI-driven personalization and IoT connections will make services even smarter, from instant credit decisions to seamless smart-device payments. As regulators fine-tune rules and cross-border tools expand, embedded finance stands ready to fuel growth across industries through 2030.

Sources:

- https://resolvepay.com/blog/17-statistics-that-explain-the-rise-of-embedded-finance-in-wholesale-e-commerce

- https://market.us/report/embedded-finance-market/

- https://www.alloy.com/blog/11-embedded-finance-stats-for-banks-2024

- https://www.absrbd.com/post/embedded-finance-statistic

- https://www.precedenceresearch.com/embedded-finance-market

- https://sdk.finance/blog/embedded-finance-solutions-how-businesses-are-integrating-financial-services/