Insurance Industry statistics: The global insurance industry has continued to expand, with worldwide premium income estimated at about EUR 7.0 trillion in 2024 after premium growth of roughly 8.6%, outpacing the strong 8.2% increase recorded in 2023. Life insurance remains the largest segment, generating around EUR 2.9 trillion in premiums in 2024, followed by property and casualty at about EUR 2.4 trillion and health insurance at nearly EUR 1.7 trillion, reflecting rising demand for both long‑term savings protection and risk transfer solutions in a volatile macroeconomic environment.

In real terms, growth is being supported by a combination of moderating inflation, rate hardening in non‑life lines, and higher interest rates that are improving investment returns, with recent analyses indicating that global life premiums are expected to grow close to 3 percent in real terms and non‑life premiums by just above 3% as claims inflation gradually eases.

At the same time, capital strength across the sector has improved, evidenced by record reinsurance dedicated capital of about USD 769 billion at the end of 2024, while technology investment in insurtech has become more selective, with funding volumes stabilizing after recent declines and a growing share of deals focused on artificial intelligence‑driven solutions that enhance underwriting, pricing, and customer engagement.

Statistical Facts

- The global insurance market is expected to reach USD 8.88 trillion in premiums by 2026, reflecting steady growth supported by life, health, and non-life insurance segments.

- North America is projected to contribute nearly 42% of global insurance premiums in 2026, maintaining its position as the leading regional market.

- The insurtech market was valued at USD 1.19 trillion in 2025 and is estimated to reach USD 1.34 trillion in 2026, with continued expansion toward USD 2.44 trillion by 2031 at a 12.72% CAGR.

- Insurtech growth is being supported by wider digital adoption, increased automation across insurance operations, and greater use of data driven decision processes.

- Global primary insurance premiums are expected to grow by around 2.0% in 2025 and 2.3% in 2026 in real terms, indicating moderate but stable market expansion.

- Non life insurance growth is likely to slow as competitive intensity increases and pricing pressure builds across key markets.

Recent Developments

- New India Assurance, 2025: Recorded record gross written premium of ₹43,618 crore, up 3.86% year-over-year, while maintaining 12.6% market share in non-life insurance. Combined ratio improved to 117% from 120%, with loss ratio at 96.61%; net profit declined 12.86% to ₹988 crore due to ₹802 crore provisions for legacy reinsurance balances, but solvency ratio strengthened to 1.91x.

- LIC India, 2025: Achieved full-year net profit of ₹48,151 crore, reflecting 18% growth, with total premium income at ₹4,88,148 crore and value of new business at ₹10,011 crore (4.47% rise). Q4 FY25 quarterly net profit surged 38.15% to ₹19,013 crore, alongside EBITDA up 44.48% to ₹22,816 crore, maintaining 57.05% market share despite slight premium dip.

- HDFC Life, 2025: Q2 FY26 net profit rose 3% to ₹448 crore, with total premium up 15% to ₹34,162 crore; individual annualized premium equivalent grew 10% to ₹6,471 crore and value of new business 10% to ₹1,818 crore at 24.5% margins. Assets under management reached ₹3,59,999 crore (11% rise), with embedded value up 14% to ₹59,540 crore and operating return on EV at 15.8%.

- Max Life Insurance, 2025: Secured claim settlement ratio of 99.40% and assets under management of ₹1,96,000 crore; annual premium equivalent stood at strong levels with solvency ratio of 1.72x, positioning as a top private life insurer focused on protection products.

- Allianz SE, 2025: Ranked second globally among life insurers by reserves and liabilities, benefiting from favorable markets with improved spreads and underwriting discipline in life segment; overall profitability supported by stable investment income amid geoeconomic fragmentation.

- Prudential Financial, 2025: Led US life insurers and ranked fourth worldwide by reserves, capitalizing on North American dominance with 15 US firms in global top 50.

- Ping An Insurance, 2025: Secured third spot globally in life reserves, driven by significant year-over-year increases in China alongside strong regional growth.

Tariff Impact on the Insurance Sector

US tariffs implemented in 2026 are driving up costs across global supply chains, leading to higher claims severity and premiums in key insurance lines like property & casualty (P&C). These effects stem from inflated prices on imported parts, materials, and labor, compounded by disruptions that delay repairs and increase fraud risks.

Auto Insurance Impacts

- Auto and homeowners insurers are facing higher claims costs due to rising prices of imported repair parts and construction materials such as lumber, which is increasing premiums and putting pressure on underwriting margins.

- Tariffs on vehicles and auto parts from Canada, Mexico, and other regions are increasing repair costs, pushing average US auto insurance premiums up by 6% to 10% by year end.

- Insurers are facing higher claims expenses due to longer repair cycles, extended rental periods, and changes in customer vehicle choices toward domestic models.

- Ongoing supply chain delays are increasing loss adjustment expenses, with claims inflation flowing directly into premium rate increases.

Property and Construction Lines

- Rising prices for steel, aluminum, lumber, and electronics are increasing rebuilding costs, leading to higher insured values and premiums across homeowners and commercial property policies.

- A 10% increase in material costs on a USD 25 million construction project adds USD 2.5 million to coverage requirements, placing pressure on builder’s risk and liability insurance lines.

- Extended material lead times are lengthening policy periods, while construction delays are increasing overall risk exposure across the property and construction insurance segments.

Regional Slowdown

Non-Life Insurance Premium Growth

- Based on data from deloitte, Global non life insurance premiums slow from 4.7% in 2024 to 2.6% in 2025F and 2.3% in 2026F, reflecting easing inflation effects and normalization of pricing.

- Advanced markets overall show a clear deceleration, with growth moving from 4.5% in 2024 to around 2.2–2.7% in 2025F and settling near 1.9% in 2026F.

- North America declines sharply from 4.7% in 2024 to 2.0% in 2025F and 1.9% in 2026F, driven by softer rate increases and improved underwriting balance.

- EMEA slows from 4.5% in 2024 to 2.7% in 2025F, before easing further to 1.9% in 2026F, reflecting competitive pricing and regulatory constraints.

- Asia Pacific advanced markets moderate from 2.9% in 2024 to 2.1% in 2025F, with a mild rebound to 2.5% in 2026F due to selective repricing.

- Emerging markets overall remain faster growing but are also slowing, declining from 5.8% in 2024 to 4.6% in 2025F and 4.1% in 2026F.

- Emerging markets excluding China reduce from 5.8% in 2024 to 3.9% in 2025F, with growth stabilizing near 4.0% in 2026F.

- Industry outlook indicates a shift toward slower real premium growth across regions as rate hardening fades and market conditions become more competitive.

Life Insurance Premium Growth

- Global life insurance premiums slow sharply from 6.1% in 2024 to 1.0% in 2025F, followed by a partial recovery to 2.4% in 2026F, indicating pressure from inflation-adjusted income and weaker savings appetite.

- Advanced markets overall experience a strong deceleration, with growth falling from 3.9% in 2024 to just 0.2% in 2025F, before improving modestly to 1.6% in 2026F.

- North America shows the most pronounced slowdown, declining from 6.0% in 2024 to -1.4% in 2025F, reflecting real premium contraction, before recovering to 1.7% in 2026F.

- EMEA moderates from 4.9% in 2024 to 1.6% in 2025F, with growth stabilizing at 1.7% in 2026F, supported by gradual normalization of household savings behavior.

- Asia Pacific advanced markets remain under pressure, moving from -1.0% in 2024 to 0.4% in 2025F, and improving slightly to 1.1% in 2026F, indicating subdued demand recovery.

- Emerging markets overall continue to outperform advanced regions despite slowing, declining from 13.1% in 2024 to 3.4% in 2025F, with a rebound to 4.9% in 2026F.

- Emerging markets excluding China remain relatively resilient, easing from 10.5% in 2024 to 4.2% in 2025F, and stabilizing at 4.4% in 2026F.

- Industry trend highlights a broad slowdown in real life insurance premium growth, driven by affordability constraints, shifting savings priorities, and cautious consumer sentiment across regions.

Workforce Statistics

- Approximately 2.7 million people were employed in global insurance brokers and agencies as of 2024.

- Employment growth in this segment was around 0.5% in 2024.

- The broader finance and insurance sector employed about 4.9 million people in the European Union in 2021.

- Turnover rates in the U.S. insurance workforce recently rose to 12–15%, up from 8–9%.

- A significant share of the industry workforce is aging, with 538,000 employees aged 55–64 and 186,000 aged 65 or older.

- A notable portion of insurance employees indicate interest in virtual work opportunities, with 58% willing to work remotely for a foreign employer.

Consumer Behavior and Insurance Product Trends

- Digital insurance adoption has grown significantly, with some studies reporting adoption increases of over 40%.

- Consumers without security breaches are 40% more likely to buy more insurance services and nearly 55% likely to recommend digital insurance.

- Increasing online engagement is driving growth in online insurance market size, from $121.23 billion in 2025 to an expected $148.86 billion in 2026.

- Study findings indicate that digital platforms are broadly accepted across demographic groups.

- Online channels are cited as influential in decision-making for simple insurance products in empirical consumer behavior research.

- Usage-based insurance markets such as UBI are expanding, with forecasts showing growth from about $43.38 billion in 2023 to $70.46 billion by 2030.

Car/Auto Insurance Statistics

- Adoption of telematics-based auto insurance is rising, with consumer acceptance increasing 33% from late 2021 to early 2022.

- The telematics market within insurance is projected to grow at a CAGR of about 21.2% from 2024 to 2029.

- Usage-based insurance market forecasts suggest growth from $43.38 billion in 2023 to $70.46 billion by 2030.

- Early reports show the global auto insurance market valued close to $942 billion in 2024.

- Technological integration with AI and digital platforms is cited as a key trend in auto insurance.

- Hybrid telematics and smartphone solutions are increasingly used for personalized risk assessment and pricing.

Business Insurance Statistics

- The business insurance market was estimated at USD 847.77 billion in 2024.

- This market is projected to grow to approximately USD 926.79 billion in 2025.

- A continued expansion is expected to reach USD 2,259.36 billion by 2035.

- Cyber insurance, an important subset of business insurance, is growing rapidly; one estimate places the global cyber insurance market value at USD 14.2 billion in 2025.

- Another projection suggests cyber insurance could reach USD 120.47 billion by 2032.

- In some regions, UK cyber insurance claims more than tripled to £197 million in 2024, reflecting rising digital risks.

Health Insurance Statistics

- Global digital health insurance markets were valued near USD 3.52 trillion in 2024.

- These markets are projected to grow to USD 10.95 trillion by 2034.

- Employer-provided health benefits such as OPD coverage showed 35% year-on-year increase in adoption.

- Policy demand in some markets reached peak levels following regulatory reforms that made policies more affordable.

- Chronic disease and preventive care coverage strongly influence health insurance choices.

- Digital and online engagement in health insurance is reported to be expanding as consumer preference shifts.

(source: coinlaw.io/

Insurance Analytics Market Overview

Key insights Summary

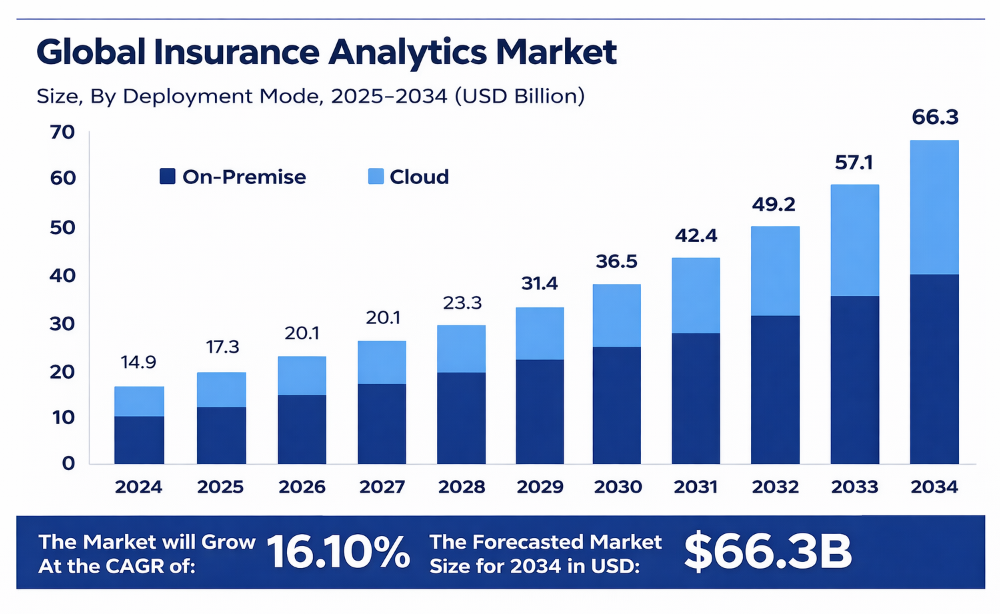

- According to Markrt.us, The global insurance analytics market generated USD 14.09 billion in 2024 and is expected to expand from USD 17.3 billion in 2025 to around USD 66.3 billion by 2034, reflecting a 16.10% CAGR over the forecast period.

- North America led the market in 2024, accounting for more than 39.2% share and around USD 5.84 billion in revenue, supported by mature insurance systems and strong adoption of digital analytics.

- By component, analytics tools held 67.3% of the market, as insurers increasingly rely on platforms that support data visualization, risk assessment, and performance monitoring.

- Claims management was the largest application area at 31.7%, driven by the use of predictive analytics to reduce fraud, improve claim accuracy, and shorten settlement timelines.

- On-premise deployment accounted for 52.2% share, reflecting continued preference for locally hosted systems to manage sensitive policyholder and customer data securely.

- Insurance companies represented 73.4% of end-user demand, highlighting sustained investment in analytics to improve underwriting quality, pricing discipline, and customer retention.

- Property and casualty insurance contributed 42.1% of total market activity, supported by the need for real-time insights to manage risk exposure and claims performance.

- Large enterprises dominated adoption with 70.2% share, as they are better positioned to integrate advanced analytics across complex and data-intensive operations.

Market Size

| Year | Market Value (USD Billion) |

|---|---|

| 2024 | 14.9 |

| 2025 | 17.3 |

| 2026 | 20.1 |

| 2027 | 23.3 |

| 2028 | 27.1 |

| 2029 | 31.4 |

| 2030 | 36.5 |

| 2031 | 42.4 |

| 2032 | 49.2 |

| 2033 | 57.1 |

| 2034 | 66.3 |

(source: market.us)

Key Applications and Benefits

- Around 86% of insurance companies use data analytics to analyze reports and gain deeper understanding of customer behavior and policy performance.

- Life insurers applying predictive analytics have reported up to 67% reduction in costs and around 60% increase in revenue, reflecting stronger operational efficiency and decision support.

- Advanced analytics supports fraud prevention, with estimated savings of over USD 300 billion annually by reducing fraudulent claims and activities.

- Micro-segmentation and price elasticity modeling enable 2% to 3% improvement in Gross Written Premium and deliver more than 85% accuracy in predicting revenue impact.

- The use of Generative AI in insurance is expected to reach about USD 8,099.97 million by 2032, growing at a 33.11% CAGR, as insurers expand automation and advanced analytics capabilities.

Agentic AI Insurance Market Overview

Key Takeaways

- The global agentic AI insurance market was valued at USD 4.60 billion in 2024 and is projected to reach USD 75.00 billion by 2034, growing at a 32.2% CAGR during the 2025 to 2034 forecast period.

- North America held a leading position in 2024, capturing more than 39.3% of the market and generating USD 1.80 billion in revenue, supported by early AI adoption and strong digital insurance ecosystems.

- Underwriting automation led the market with 37.5% share, driven by wider use of AI systems to streamline risk assessment and accelerate policy issuance.

- The life insurance segment accounted for 34.6%, reflecting growing adoption of intelligent agents to support personalized offerings and long term policy management.

- Cognitive agents represented 32.2% of the market, highlighting their role in automating decision making, customer interactions, and claims handling through adaptive learning models.

- On-premise deployment accounted for 58.9%, underscoring insurer preference for greater control over sensitive data and regulatory compliance.

- Insurance carriers held 38.9% share, supported by increased integration of agentic AI to improve operational efficiency and customer engagement.

- The US market reached USD 1.55 billion in 2024 and is expanding at a 17.3% CAGR, driven by advanced AI use across underwriting, risk modeling, and policy servicing.

AI Agent Statistics

- As of mid 2024, around 76% of US insurance companies had implemented generative AI in at least one business function, while only 10% had achieved deployment at scale, indicating a gap between pilots and enterprise wide adoption.

- Full AI adoption among insurers increased from 8% in 2024 to 34% in 2025, reflecting a 26 percentage point year over year rise in AI agent integration across insurance operations.

- Claims processing has shown the strongest impact, with resolution times reduced by 75%, falling from 30 days to 7.5 days. Routine claims are now processed within 24 to 48 hours, compared with 7 to 10 days previously.

- Policy coverage verification time has been reduced by nearly 99%, dropping from 15 to 20 minutes to only a few seconds.

- About 64% of insurers prioritize using AI to process unstructured data and documents, positioning claims management as the most mature and widely adopted application area.

- Overall, AI driven claims automation has reduced processing time by 55% to 75%, while routine claim workflows show 75% to 85% time savings, confirming claims processing as a high return use case for near term operational gains.

You Might Like

- Digital Banking Statistics: By Market, Usage and Security Insights

- Creator Economy Statistics and Insight

- Cybersecurity Statistics : Facts And Figures

- EdTech Statistics: Redefining Education in the Digital Age

- Podcast Statistics: Market to Reach USD 233.9 billion by 2032

- eSports Statistics – By Market Size, Viewers and Demographics

- DeepSeek Statistics and Latest Facts 2025

- Embedded Finance Statistics: Market Size and Adoption

Conclusion

The insurance industry continues to demonstrate steady usage growth and widening adoption across regions, supported by rising risk awareness, regulatory enforcement, and economic expansion. Global insurance penetration remains uneven, with developed regions such as North America and Europe showing high adoption levels, while emerging markets continue to display lower penetration but stronger long-term potential. This gap highlights both structural differences and untapped demand across regions.

From a line-of-business perspective, life insurance maintains a stable role in long-term financial protection, particularly in mature economies, while non-life insurance shows stronger short-term momentum driven by motor, health, and property lines. Claims inflation, medical cost increases, and climate-related losses are reshaping underwriting priorities and pricing strategies across these segments.

Looking ahead, technology adoption, sustainability-focused risk assessment, and evolving regulatory frameworks are expected to play a central role in shaping the industry’s direction. Greater use of data analytics, automation, and customer-focused product design is supporting improved coverage accessibility and operational stability. Overall, the industry is positioned to grow steadily while balancing profitability, compliance, and emerging risk exposure.

Sources:

- https://www.fortunebusinessinsights.com/cyber-insurance-market-106287

- https://www.mordorintelligence.com/industry-reports/global-insurtech-market

- https://www.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/insurance-industry-outlook.html

- https://coinlaw.io/insurance-industry-statistics/

- https://market.us/report/agentic-ai-insurance-market/