Embedded Lending vs. Embedded Finance

Embedded lending focuses on loans and credit options built right into non-financial apps, like buy-now-pay-later at checkout. Embedded finance goes wider, adding payments, insurance, and banking to those same platforms for a full financial setup. Lenders need to grasp this split to pick the right path for their business.

Core Ideas

Embedded lending lets users grab credit without leaving the app they use, say for shopping or SaaS tools. It relies on APIs for quick checks on credit using platform data, then dishes out funds on the spot. Think point-of-sale loans in retail that boost sales by easing big buys.

Embedded finance wraps in more than just loans. It covers payments like digital wallets, insurance at purchase, and even bank accounts in one place. Platforms like ride-sharing apps add payouts or cards for drivers, making finance feel part of the main service.

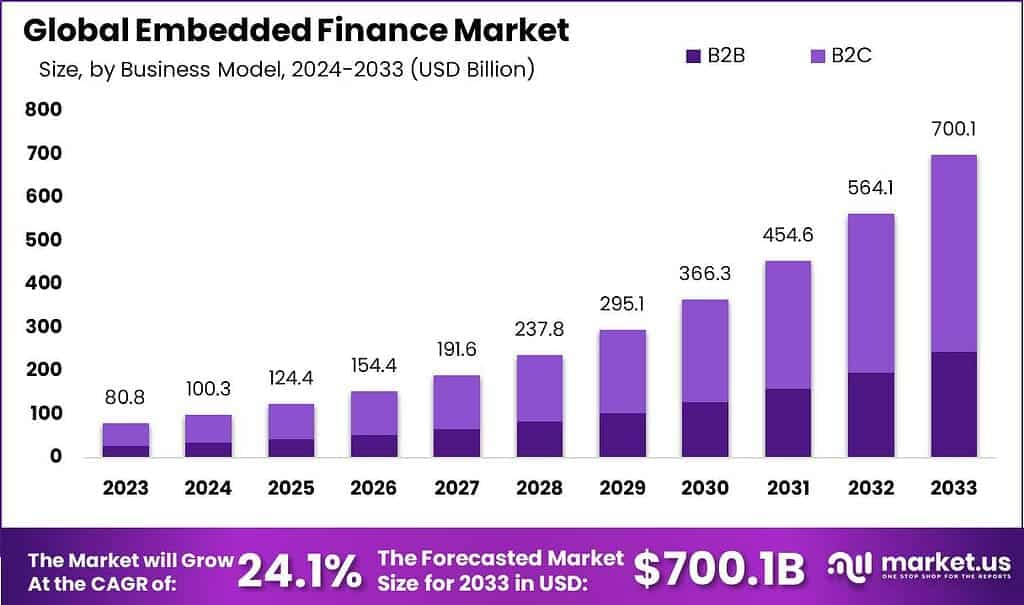

Key Statistics for Embedded Finance

- According to Market.us, The global embedded finance market is expected to reach USD 700.1 billion by 2033, up from USD 80.85 billion in 2023, growing at a 24.10% CAGR from 2024 to 2033.

- In 2023, North America held over 35% share, generating USD 28.3 billion in revenue.

- Companies adopting embedded financial services report a 15% to 20% increase in revenue.

- Customer retention improves by 22% when embedded finance is integrated.

- 64% of businesses plan to launch embedded finance solutions in 2025.

- The retail and e-commerce sector accounts for the largest share with 36.47% in 2024.

- North America is the largest market, while Asia Pacific is the fastest-growing, projected to expand at 26.45% CAGR through 2030.

(source: market.us)

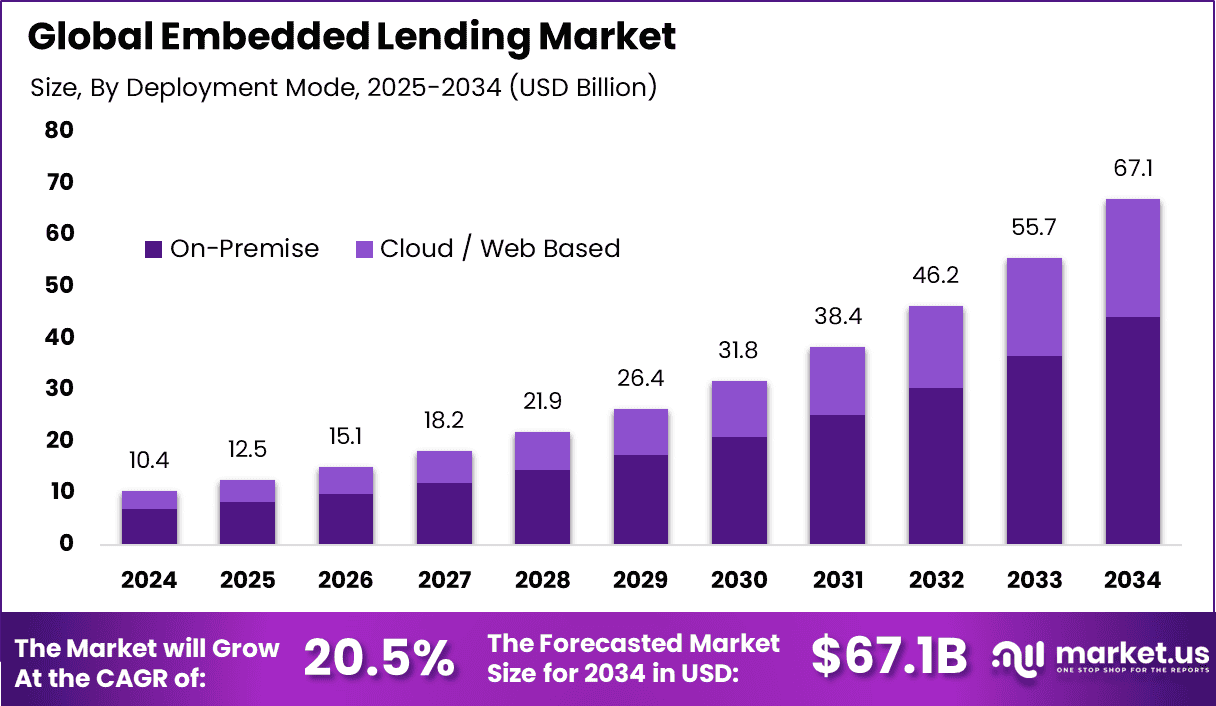

Key Statistics for Embedded Lending

- The global embedded lending market generated USD 10.4 billion in 2024.

- Revenue is set to grow from USD 12.5 billion in 2025 to USD 67.1 billion by 2034, reflecting a 20.5% CAGR.

- In 2024, North America captured 37.4%, generating USD 3.3 billion in revenue.

- Embedded lending is seen as the most disruptive segment within embedded finance.

- More than 40% of consumers are willing to switch to platforms offering embedded lending.

- 56% of Gen Z and 55% of millennials have strong interest in embedded lending services.

- In India, embedded lending holds about 35% of the digital lending market.

- AI and alternative data technologies help significantly reduce loan processing costs, enabling viable small-ticket lending.

(source: market.us)

Main Differences

| Aspect | Embedded Lending | Embedded Finance |

|---|---|---|

| Focus | Loans, BNPL, credit lines | Payments, insurance, banking, and loans |

| Common Spots | E-commerce, B2B sites | Apps, neobanks, full platforms |

| Tech Needs | Loan APIs, origination software | BaaS, SDKs for all services |

| Partners | Retailers, POS systems | Software firms, payment networks |

Real-World Uses

- Retail picks embedded lending for BNPL or store financing, like splitting sofa costs at Jerome’s Furniture. This lifts order sizes and keeps buyers coming back.

- E-commerce platforms embed loans for sellers to stock up or run ads, smoothing cash flow in spots like Flipper.

- Gig apps like Uber offer driver loans or cards via embedded finance, tying rewards to ride data for quick cash.

- B2B SaaS uses lending for supplier payments, while finance adds virtual cards for spend control.

2025 Trends to Watch

- Increased API Standardization: More standardized API ecosystems are emerging, making embedding multiple financial services easier and more secure.

- AI and Data Analytics: AI drives personalized financing and financial products embedded directly based on user behavior and creditworthiness.

- Expansion into New Markets: Embedded finance and lending are expanding into emerging markets with mobile-first strategies leading adoption.

- Partnerships and Ecosystem Building: Fintechs, traditional banks, and tech platforms increasingly form partnerships to build end-to-end embedded solutions.

- Regulatory Evolution: Regulators are focusing more on embedded finance transparency, consumer protection, and anti-fraud measures, which shape product design.

Applications

Embedded finance encompasses various applications beyond lending:

- Payment processing within apps or websites, improving user checkouts without redirecting to external financial institutions.

- Insurance offers closely tied to user activities, such as travel insurance bought during trip bookings.

- Payroll, invoicing, and financial management tools embedded in SaaS platforms for business users.

Embedded lending’s applications are particularly prominent in:

- E-commerce platforms integrating BNPL solutions to boost sales and average order values.

- SaaS platforms providing instant credit or working capital loans tailored to customer business needs.

- Marketplace and gig economy platforms offering seamless credit to workers or sellers at points of transaction.

Market Impact

Embedded lending boosts sales conversion and customer loyalty for merchants by reducing financing barriers at the point of purchase. For consumers, it offers more immediate access to affordable credit.

Embedded finance, meanwhile, redefines the entire customer experience, enabling seamless financial interactions that keep users within an ecosystem longer. Together, these technologies drive financial inclusion and spur innovation in retail, transportation, gig work, and more.

Future Trends and Challenges

Both embedded lending and finance markets are poised for rapid growth, driven by evolving customer expectations for speed, personalization, and convenience. AI and advanced data analytics will continue transforming lending processes with enhanced credit risk assessments, automated underwriting, and proactive customer management.

Regulatory compliance and data privacy amid varying global standards remain significant challenges requiring ongoing collaboration between fintech providers, lenders, and regulators. Technological advances like Lending-as-a-Service (LaaS) platforms also offer scalability and ease of integration, helping new players enter the embedded lending space flexibly.

Conclusion

In conclusion, embedded lending represents a critical, focused slice of the larger embedded finance landscape. Both continue to grow in tandem in 2025, powered by advanced technology, evolving regulation, and the demand for integrated, hassle-free financial experiences. Companies embedding these services strategically position themselves for stronger customer engagement and new revenue streams.

You May also like this

- AI Agents Statistics: Market Size, Adoption Rate and Trends

- Voice AI Agents Statistics, Market Size and Adoption Trends

- Streaming Services Statistics by Category and Emerging Trends

- Top Drone Companies Shaping Global Market Growth

- Statistical Analysis of the Insurance Industry

Sources:

- https://stripe.com/in/resources/more/open-banking-vs-embedded-finance-a-guide

- https://staxpayments.com/blog/embedded-finance/

- https://pipe.com/resources/articles/exploring-the-benefits-of-embedded-lending

- https://www.pwc.com/gx/en/issues/technology/tech-translated-embedded-finance.html