Semiconductor Statistics: The semiconductor industry refers to the global industry that designs, manufactures, and supplies semiconductor devices such as microprocessors, memory chips, sensors, power devices, and integrated circuits. These components are foundational to modern electronics and are embedded in a wide range of products including smartphones, computers, automobiles, industrial equipment, medical devices, and consumer appliances. The semiconductor industry supports digital transformation across sectors by enabling data processing, connectivity, energy management, artificial intelligence, and advanced automation.

Top Editor’s Choice

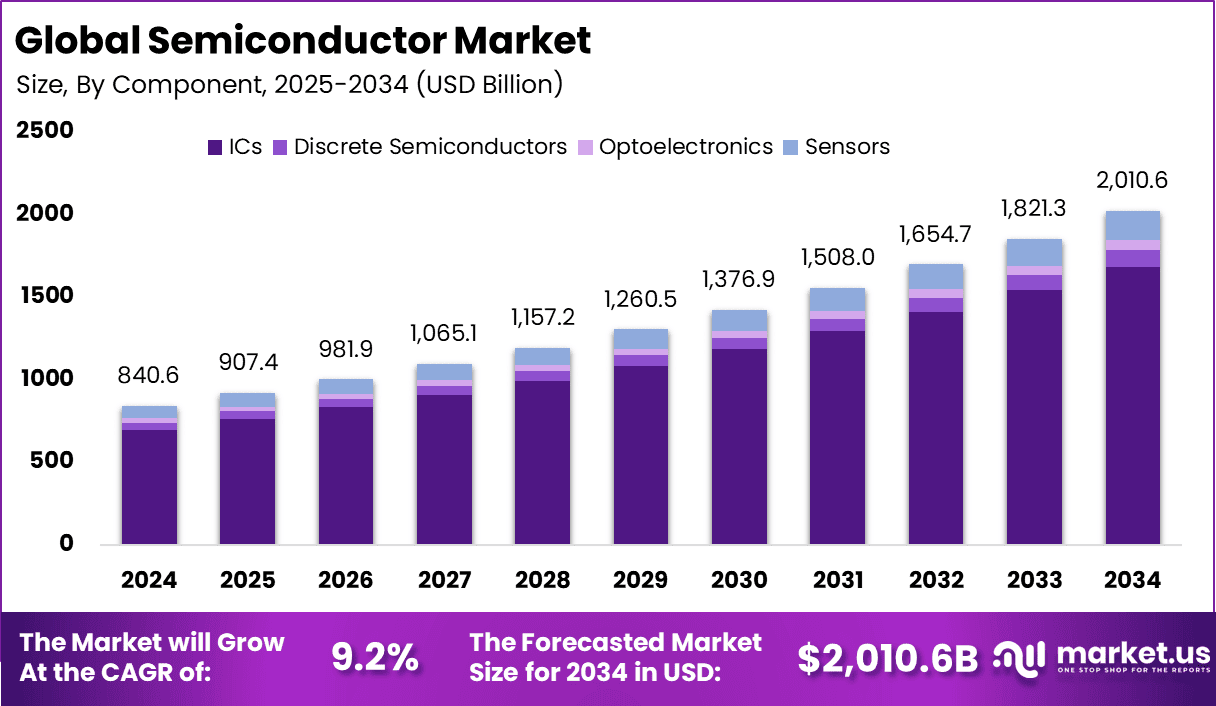

- According to Market.us, The global semiconductor market reached USD 840.60 billion in 2024. This growth reflects strong demand from electronics, automotive, and industrial sectors. The market is expected to rise from USD 907.4 billion in 2025 to nearly USD 2,010.6 billion by 2034. A steady 9.20% CAGR is projected during the forecast period.

- China plans to invest USD 150 billion in its semiconductor industry by 2025, aiming to strengthen domestic chip production.

- Global semiconductor sales are expected to reach USD 588.36 billion in 2024, showing steady industry demand.

- Memory semiconductor revenue is estimated at USD 129.8 billion in 2024, up 44.8% from 2023, driven by AI and data center demand.

- Nvidia leads the semiconductor sector by market value at USD 2.20 trillion, followed by TSMC at USD 714.45 billion and Broadcom at USD 573.81 billion.

- Shipments of edge AI chips in smartphones are projected to reach 1 billion units in 2024, highlighting rapid on-device AI adoption.

- Global semiconductor capital spending is forecast at USD 146.6 billion, down 19% year over year, reflecting cautious investment cycles.

- Global semiconductor sales reached $72.7 billion in October 2025, reflecting strong monthly performance.

- Sales increased by 4.7% compared to September 2025, when the market recorded $69.5 billion in revenue.

- On a year-on-year basis, October 2025 sales were 27.2% higher than October 2024, which stood at $57.2 billion.

- Monthly semiconductor sales figures are calculated using a three-month moving average, compiled by the World Semiconductor Trade Statistics (WSTS) organization.

- The Semiconductor Industry Association (SIA) represents 99% of the U.S. semiconductor industry by revenue, indicating broad industry coverage.

- SIA members also account for nearly two-thirds of non-U.S. semiconductor companies, highlighting its global industry representation.

Recent Developments

- August 2025: Ainos signed a three year subscription agreement valued at USD 2.1 million with ASE Technology Holding Co. Under this agreement, 1,400 AI Nose units were deployed across three semiconductor manufacturing facilities in Taiwan. This marked the first industrial deployment of Ainos’ scent digitization platform within a chip manufacturing environment, highlighting its role in factory monitoring and process control.

- August 2025: Following the public announcement of the AI Nose agreement, Ainos’ stock price increased by just over 50%. This movement reflected strong investor response to the company’s first major industrial revenue stream. The deal also strengthened confidence in the commercial scalability of Ainos’ SmellTech as a Service platform for semiconductor manufacturing applications.

- August 2025: Taiwan Semiconductor Manufacturing Co. announced a USD 100 billion investment plan in the United States. The expansion included three fabrication plants, two advanced packaging facilities, and a research and development center in Arizona. The initiative was aimed at reducing supply chain risks while generating thousands of union jobs in the U.S. market.

- August 2025: Former President Trump announced a 100% tariff on imported semiconductors, with exemptions for companies manufacturing or operating facilities in the United States. The policy was designed to encourage domestic chip production and retain semiconductor related tax revenue. This measure supported increased onshore manufacturing by companies such as Apple and TSMC.

Semiconductor Market Size Statistics

- Integrated Circuits (ICs) dominated the global semiconductor market in 2024, accounting for over 83.1% of total demand.

- Networking and communications emerged as the leading application segment, capturing more than 37.8% market share, supported by 5G, data traffic growth, and cloud infrastructure expansion.

- China’s semiconductor market reached a value of USD 265.2 billion in 2024, reflecting strong domestic production and consumption momentum, with a steady 8.6% CAGR outlook.

- Asia Pacific led the global semiconductor market with over 65.7% share, driven by its strong manufacturing base, advanced foundry ecosystem, and high electronics production across China, Taiwan, South Korea, and Japan.

(image credit: market.us)

Impact of AI on Semiconductor

AI drives massive demand for advanced chips in the semiconductor industry, especially for data centers and generative AI models, while also speeding up design and manufacturing processes. Top companies like Nvidia and TSMC capture most gains, but smaller players struggle with high costs and supply issues as of late 2025. This creates a split market where AI boosts overall growth yet squeezes many firms amid geopolitical tensions and inventory buildup.

Key Statistics

- Top 5% of companies generated $147 billion in economic profit in 2024, while middle 90% made just $5 billion and bottom 5% lost $37 billion.

- Semiconductor industry economic profit hit $473 billion from 2020-2024, up from $450 billion in 2010-2019, fueled by AI and pandemic shortages.

- AI-related segments grew at 21% CAGR from 2019-2023, versus 6% for overall industry (9% excluding memory).

- Supplier inventory levels stood at 58-69% of next-quarter revenue in Q3 2024, signaling slow recovery outside top players.

- China’s share of global semiconductor equipment sales rose to 38% in 2024 from 6% in 2010.

Semiconductor Industry Performance

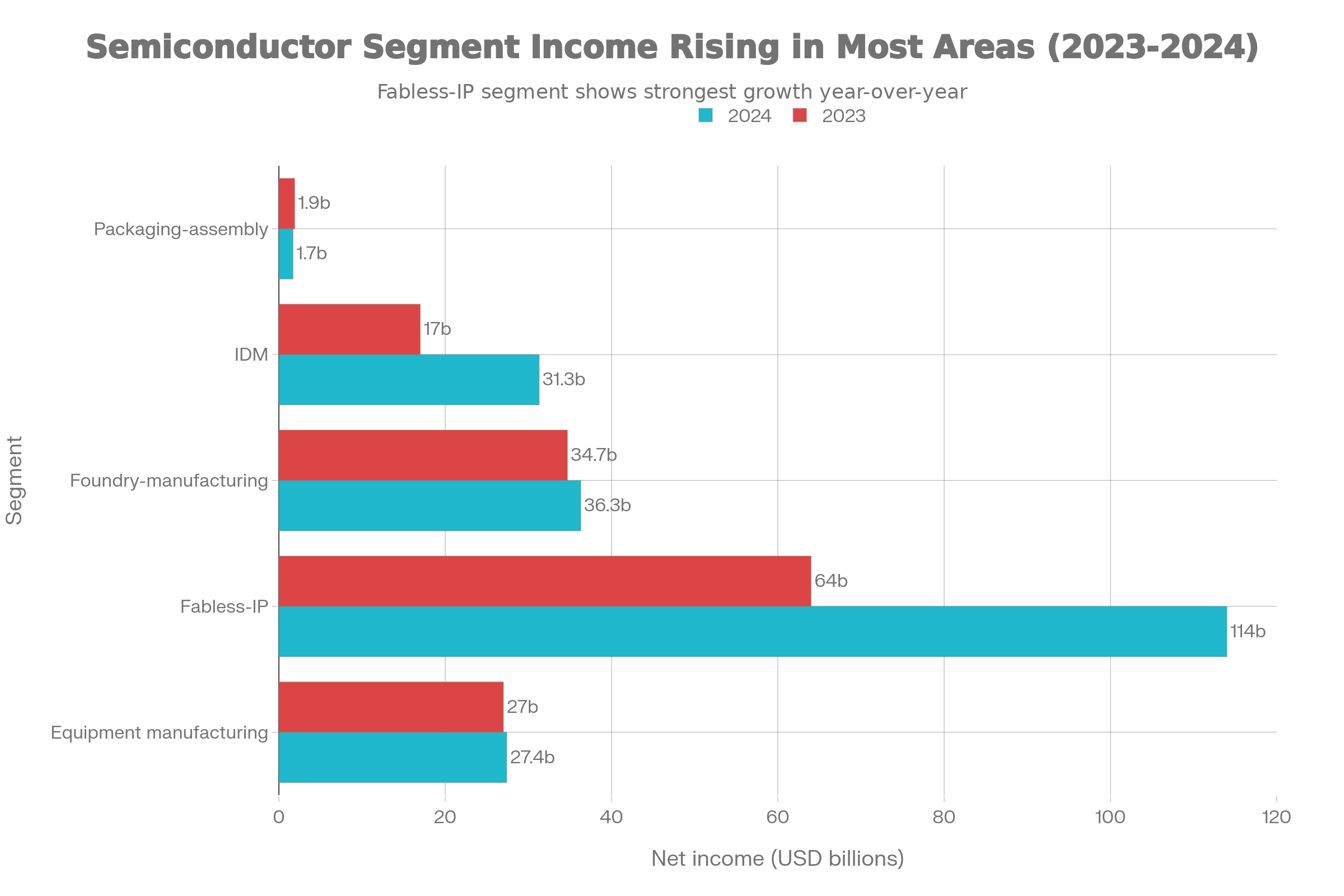

- Equipment Manufacturing recorded stable performance. Net income increased slightly from $27.0 billion in 2023 to $27.4 billion in 2024, indicating steady demand for fabrication tools and process equipment.

- Fabless and IP companies delivered the strongest growth. Net income rose sharply from $64.0 billion in 2023 to $114.0 billion in 2024, driven by high demand for AI processors, GPUs, and a

- dvanced chip designs.

- Foundry Manufacturing showed modest improvement. Net income increased from $34.7 billion in 2023 to $36.3 billion in 2024, supported by higher utilization rates and demand for advanced nodes.

- Integrated Device Manufacturers (IDMs) experienced significant recovery. Net income climbed from $17.0 billion in 2023 to $31.3 billion in 2024, reflecting improved pricing, better capacity utilization, and recovery in end-market demand.

- Packaging and Assembly revenues softened slightly. Net income declined from $1.9 billion in 2023 to $1.7 billion in 2024, suggesting margin pressure despite steady shipment volumes.

(image credit: infosys.com)

Regional Analysis

- The Asia Pacific semiconductor market reached USD 346.96 billion in 2024, highlighting the region’s dominant role in the global chip industry.

- Asia Pacific remains the largest semiconductor manufacturing and consumption hub, supported by strong presence of foundries, OSAT providers, and electronics manufacturing clusters.

- The region benefits from high concentration of chip production, including logic, memory, and power semiconductors, which supports large-scale supply to global markets.

- Strong demand from consumer electronics, data centers, automotive electronics, and industrial automation continues to support market expansion across Asia Pacific.

- Government support for local semiconductor manufacturing, technology self-reliance, and supply chain localization is further strengthening the region’s market position.

- Asia Pacific also plays a critical role in export-oriented semiconductor supply, serving North America and Europe with advanced and mature-node chips.

(image credit: fortunebusinessinsights.com)

Semiconductor Market Share by country (%), 2020-2024

| By Country | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| China | 49.8% | 49.3% | 48.9% | 48.5% | 48.0% |

| Japan | 15.1% | 15.2% | 15.2% | 15.3% | 15.3% |

| South Korea | 8.8% | 8.7% | 8.7% | 8.7% | 8.6% |

| India | 9.8% | 10.2% | 10.5% | 10.9% | 11.2% |

| Australia | 3.8% | 3.7% | 3.7% | 3.7% | 3.6% |

| Singapore | 3.9% | 4.0% | 4.1% | 4.2% | 4.3% |

| Thailand | 2.3% | 2.4% | 2.4% | 2.4% | 2.4% |

| Vietnam | 2.9% | 3.2% | 3.4% | 3.2% | 3.1% |

| Rest of Asia Pacific | 3.6% | 3.6% | 3.5% | 3.4% | 3.4% |

(data source: market.us)

Key Investments

- U.S. semiconductor ecosystem announced over $500 billion in private investments by July 2025.

- Global fab investments projected at $1.5 trillion from 2024-2030, half for AI and EVs.

- Nvidia invested $5 billion in Intel for data center CPU partnership in September 2025.

- AI chip startups raised $2.5 billion in 2025, up 89% year-over-year.

- Compute segment of semiconductors to hit $349 billion in 2025, growing 36%.

Partnerships like OpenAI with AMD for 6 gigawatts of AI chips starting 2026 and Broadcom for accelerators show tight integration across the stack. These moves help firms like TSMC and Samsung lock in orders while challenging Nvidia’s lead, though geopolitical rules slow some flows.

Major Collaborations

- Nvidia-Intel: $5B stake plus high-speed chip interconnects for AI servers.

- OpenAI-AMD: Multi-year deal for AI capacity, option for 10% shares.

- OpenAI-Broadcom: Custom accelerators and networks for AI clusters.

- TSMC pitched foundry JVs to Nvidia, AMD, Broadcom for Intel turnaround.

- AMD-Broadcom-TSMC: Custom AI chip design and fabrication.

Issues, Priorities, and Expectations

Industry Issues and Strategic Priorities

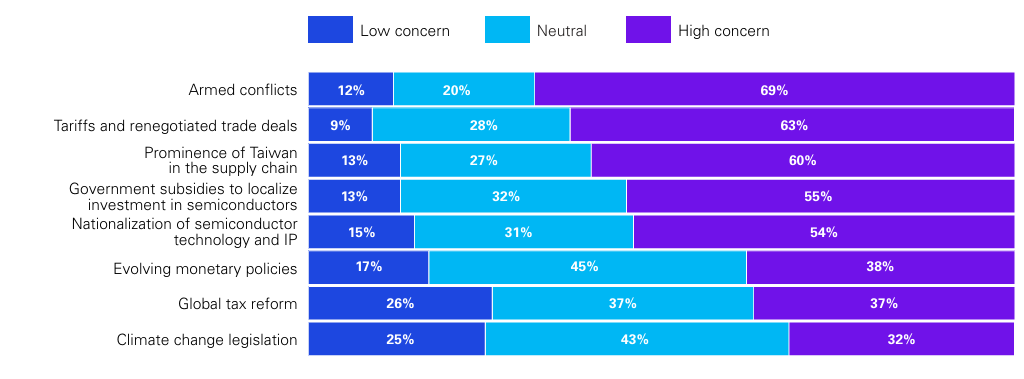

Territorial risks, tariffs, and talent shortages are identified as the biggest issues facing the semiconductor industry over the next three years. These risks are expected to influence sourcing decisions, fab location strategies, and cross-border trade stability. Talent risk remains high as advanced chip design, manufacturing, and AI skills remain in limited supply.

Supply chain flexibility and talent development and retention are ranked as the top strategic priorities for the next three years. These priorities are closely followed by digital transformation and the adoption of generative artificial intelligence. The focus reflects the need to balance operational resilience with innovation speed in an increasingly complex market.

| Key Issue | Share (%) |

|---|---|

| Talent risk including shortage of skilled workers | 40% |

| Territorialism, tariffs, and trade restrictions | 40% |

| Supply chain disruption | 35% |

| Increasing research and development costs | 26% |

| High foundry cost | 24% |

| Excess semiconductor production capacity | 21% |

| Government subsidies to localize semiconductor investments | 20% |

| Semiconductor production capacity constraints | 19% |

| Global inflation and government policy responses | 19% |

| Average selling price erosion | 17% |

| Cybersecurity risks | 16% |

| Other factors | 1% |

(data source: kpmg.com)

As non-traditional semiconductor players such as technology companies, platform providers, and automotive manufacturers expand their chip capabilities, competitive pressure is rising. Industry leaders indicate strong concern that new entrants will intensify competition for skilled engineers and specialized talent, increasing hiring costs and retention challenges across the sector.

(image source: kpmg.com)

Financial Expectations

Revenue sentiment remains highly positive across the semiconductor industry. Around 86% of executives expect their company revenue to grow in 2025, supported by strong demand from AI, data infrastructure, and automotive electronics.

Investment activity is also expected to remain strong. About 63% of companies plan to increase semiconductor capital spending, reflecting continued expansion of fabrication capacity and equipment upgrades. At the same time, 72% of respondents predict an increase in research and development spending, highlighting the importance of innovation, advanced nodes, and performance optimization.

Growth Applications and Product Trends

Microprocessors, including GPUs, are ranked as the top product opportunity for industry growth over the next year. These products are seeing sustained demand due to AI training, inference workloads, and high-performance computing applications.

Artificial intelligence has become the number one application driving semiconductor revenue for the first time. Cloud and data center applications have moved to second place, indicating a shift in demand toward AI-specific architectures. Automotive applications continue to play a major role, maintaining their position as a leading growth driver for the second consecutive year.

Operational Expectations

Increasing geographical diversity is identified as the top operational change companies plan to make to strengthen supply chain agility and resilience. Expanding sourcing and manufacturing across multiple regions is seen as a critical response to geopolitical uncertainty and regional disruptions.

Inventory optimization is another major operational focus. Reducing on-hand inventory levels is ranked as the number one response to the current economic environment. At the same time, 29% of industry participants report that excess semiconductor inventory already exists, while 25% believe demand will align with supply over the next four years, supported by the adoption of emerging technologies and new end-use applications.

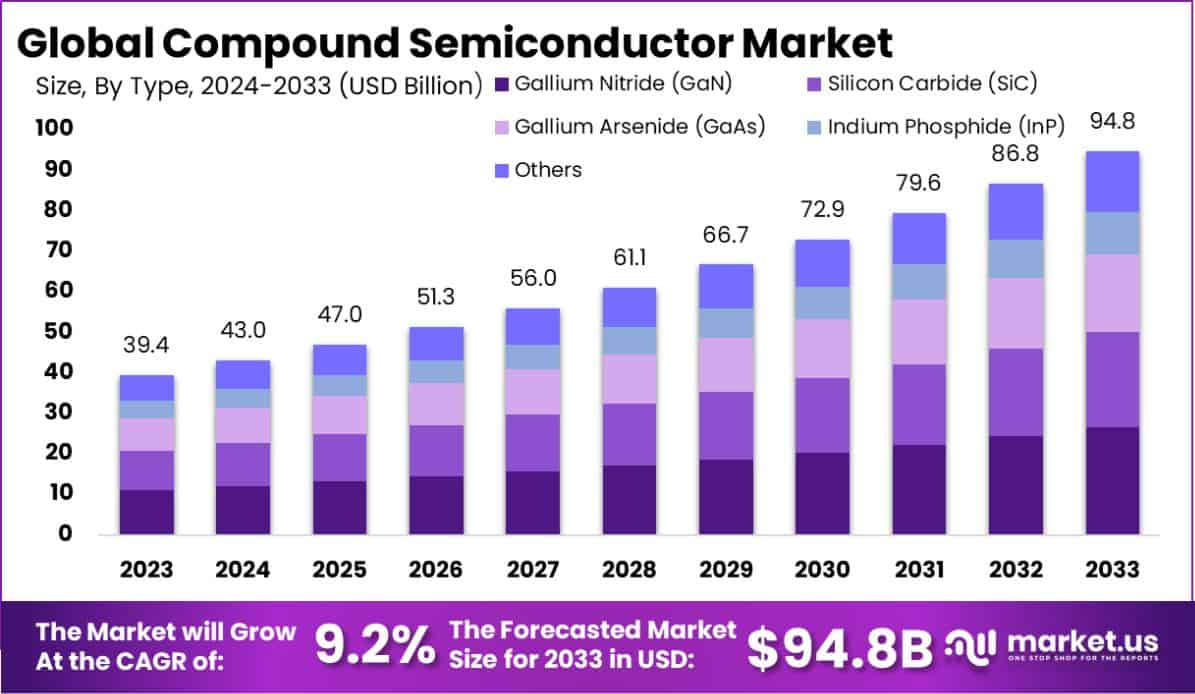

Compound Semiconductor Market Size

- The global compound semiconductor market is projected to reach USD 94.8 billion by 2033, rising from USD 39.4 billion in 2023, supported by a steady 9.2% CAGR during 2024–2033.

- Gallium Nitride (GaN) led the market by type in 2023, capturing over 28% share, driven by its efficiency in power electronics and high-frequency applications.

- LEDs dominated the product segment with more than 35% share, reflecting strong demand from lighting, displays, and automotive applications.

- IT and Telecom emerged as the largest application segment, accounting for over 40% share, supported by 5G rollout, data centers, and network infrastructure expansion.

- Asia Pacific remained the leading regional market with 55% share in 2023, generating USD 21.68 billion in revenue, driven by strong manufacturing capacity and electronics demand across China, Japan, South Korea, and Taiwan.

(image credit: market.us)

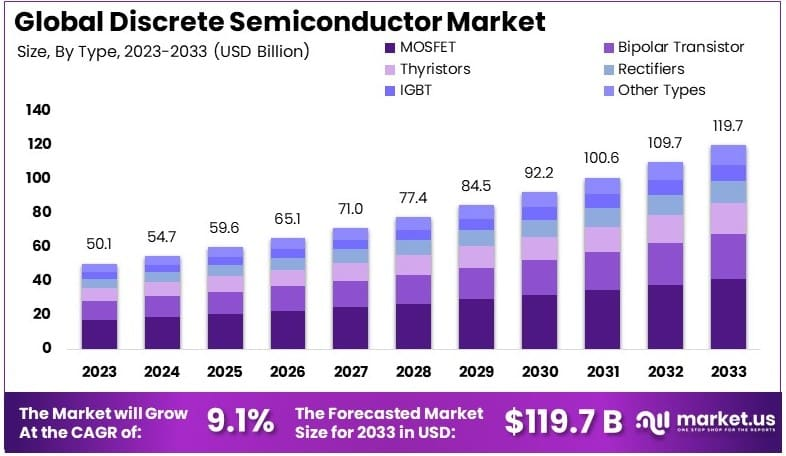

Discrete Semiconductor Market Size

- The discrete semiconductor market was valued at USD 50.1 billion in 2023 and is projected to reach USD 119.7 billion by 2033, growing at a 9.1% CAGR over the forecast period.

- MOSFETs led the type segment with a 34.5% share, supported by their wide use in power management, switching, and energy-efficient electronic devices.

- Consumer electronics emerged as the largest end-use industry, accounting for 35.1% share, driven by rising demand for compact, reliable, and low-power components.

- Bipolar transistors continued to show strong growth due to their importance in high-current and high-reliability applications.

- Thyristors maintained a stable market presence, remaining essential for high-voltage and high-power industrial systems.

- Asia-Pacific dominated the global market with a 44.0% share, supported by strong manufacturing activity in consumer electronics and automotive sectors.

(image credit: market.us)

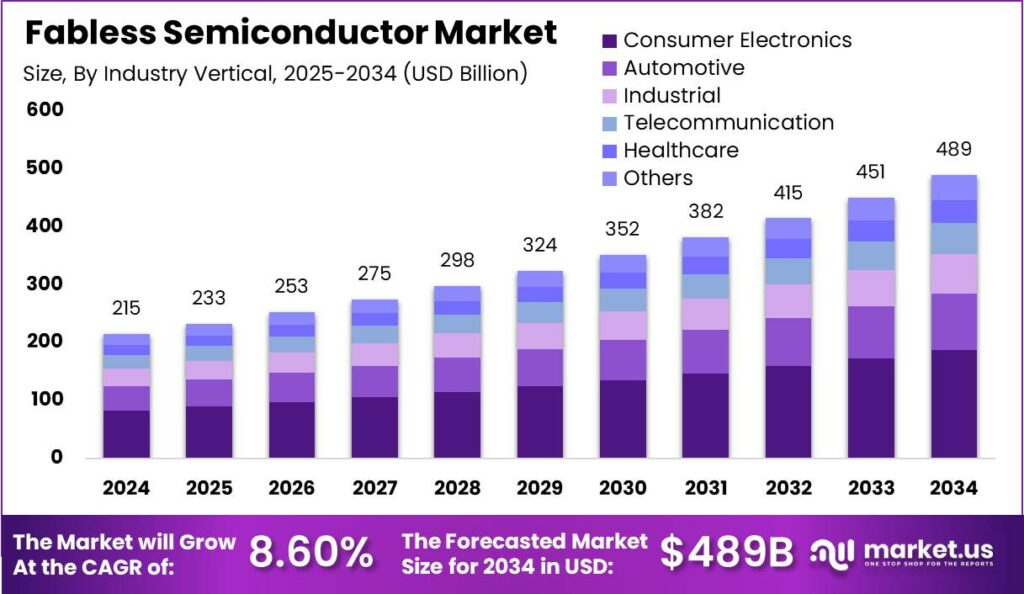

Fabless Semiconductor Market Size

- The global fabless semiconductor market is expected to reach USD 489 billion by 2034, rising from USD 214.5 billion in 2024, growing at a CAGR of 8.60% during the forecast period.

- Application Specific Integrated Circuits (ASICs) dominated the market in 2024 with a 42.84% share, driven by demand for customized and high-performance chip designs.

- Consumer electronics emerged as the leading application, capturing 38.3% of market share, supported by strong demand for smartphones, wearables, and smart devices.

- Asia-Pacific led the global market with a 58.61% share in 2024, generating around USD 125 billion in revenue, supported by a strong electronics manufacturing ecosystem.

- The China fabless semiconductor market was valued at USD 43.62 billion in 2024 and is projected to grow at a CAGR of 8.72%, driven by domestic chip design capabilities and government support.

(image credit: market.us)

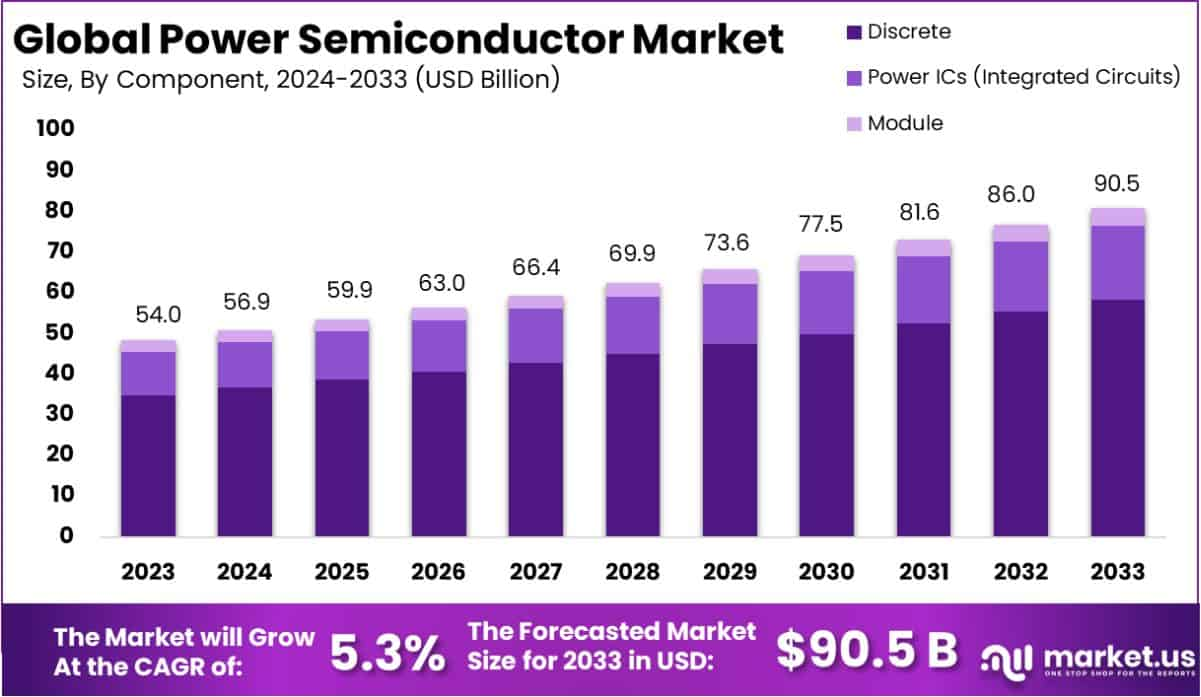

Power Semiconductor Market Size

- The global power semiconductor market is projected to reach USD 90.5 billion by 2033, up from USD 54.0 billion in 2023, growing at a CAGR of 5.3% during the forecast period.

- Discrete components dominated the market in 2023 with a 64.5% share, as they remain widely used in power control, switching, and voltage regulation applications.

- Silicon Carbide (SiC) led the material segment with a 68.1% share, driven by its superior efficiency, high-temperature tolerance, and rising adoption in EVs and renewable energy systems.

- Consumer electronics emerged as the largest end-use industry, capturing 28.0% of market share, supported by strong demand for smartphones, home appliances, and power-efficient devices.

- Asia Pacific held the leading regional position with a 45.3% market share in 2023, generating USD 24.46 billion in revenue, backed by large-scale electronics manufacturing and growing EV production.

(image credit: market.us)

Investment Opportunities

Investment opportunities exist across semiconductor design, manufacturing equipment, materials, packaging technologies, and specialized IP cores. Growth in artificial intelligence, edge computing, and automotive electrification creates demand for tailored semiconductor solutions.

Emerging regions investing in semiconductor fabrication capacity present opportunities for diversification of supply chains. Startups and technology innovators focused on low power designs, advanced nodes, and application specific integrated circuits (ASICs) are areas of active funding and strategic partnerships.

Business Benefits

Semiconductor integration delivers measurable business benefits through improved product performance, reliability, and competitive differentiation. Efficient chip designs reduce energy consumption and extend product lifecycles. High quality semiconductors support customer satisfaction by enabling feature rich and responsive user experiences. For manufacturers, using advanced semiconductor solutions can improve system throughput and support scalability for future software and hardware upgrades.

Future Outlook and Opportunities

The future outlook for the semiconductor market remains strong as digital infrastructure, connected systems, and intelligent technologies continue to expand. Areas such as artificial intelligence acceleration, quantum computing components, and energy efficient edge devices will shape future semiconductor demand.

Continued innovation in chip architectures and manufacturing methods will enable new applications in healthcare, autonomous systems, industrial automation, and advanced communication networks. As technology adoption broadens globally, semiconductors will remain a foundational element of digital progress.

Conclusion

The semiconductor market remains a fundamental pillar of the global digital economy. Its importance continues to expand as industries adopt advanced computing, connectivity, and automation technologies. Semiconductors enable progress across consumer electronics, industrial systems, automotive platforms, healthcare equipment, and digital infrastructure. Continuous innovation in chip design, manufacturing processes, and integration methods has strengthened performance, efficiency, and reliability across applications.

Looking ahead, sustained demand from artificial intelligence, data centers, electric mobility, and connected devices is expected to reinforce the strategic value of semiconductors. Supply chain resilience, investment in advanced manufacturing, and focus on energy efficient designs will remain critical priorities. Overall, semiconductors will continue to shape technological advancement, support economic growth, and serve as a core enabler of future digital transformation across global markets.

You may also read:

Sources:

- https://www.infosys.com/iki/research/semiconductor-industry-outlook2025.html

- https://kpmg.com/kpmg-us/content/dam/kpmg/pdf/2025/global-semiconductor-industry-outlook-2025.pdf

- https://www.precedenceresearch.com/semiconductor-markethttps://coolest-gadgets.com/semiconductor-industry-statistics/

- https://www.semiconductors.org/global-semiconductor-sales-increase-4-7-month-to-month-in-october/

- https://www.semiconductors.org/wp-content/uploads/2025/07/SIA-State-of-the-Industry-Report-2025.pdf

- https://aimagazine.com/news/pwc-semiconductor-fab-investment-to-hit-us-1-5tn-by-2030

- https://openai.com/index/openai-and-broadcom-announce-strategic-collaboration/

- https://www.reuters.com/world/asia-pacific/nvidia-bets-big-intel-with-5-billion-stake-chip-partnership-2025-09-18/

- https://finance.yahoo.com/news/tsmc-becomes-ai-backbone-nvidia-121644469.htmlhttps://my.idc.com/getdoc.jsp?containerId=prUS53791725

- https://www.reuters.com/world/asia-pacific/nvidia-bets-big-intel-with-5-billion-stake-chip-partnership-2025-09-18/

- https://market.us/report/power-semiconductor-market/

- https://market.us/report/fabless-semiconductor-market/

- https://market.us/report/compound-semiconductor-market/

- https://market.us/report/discrete-semiconductor-market/