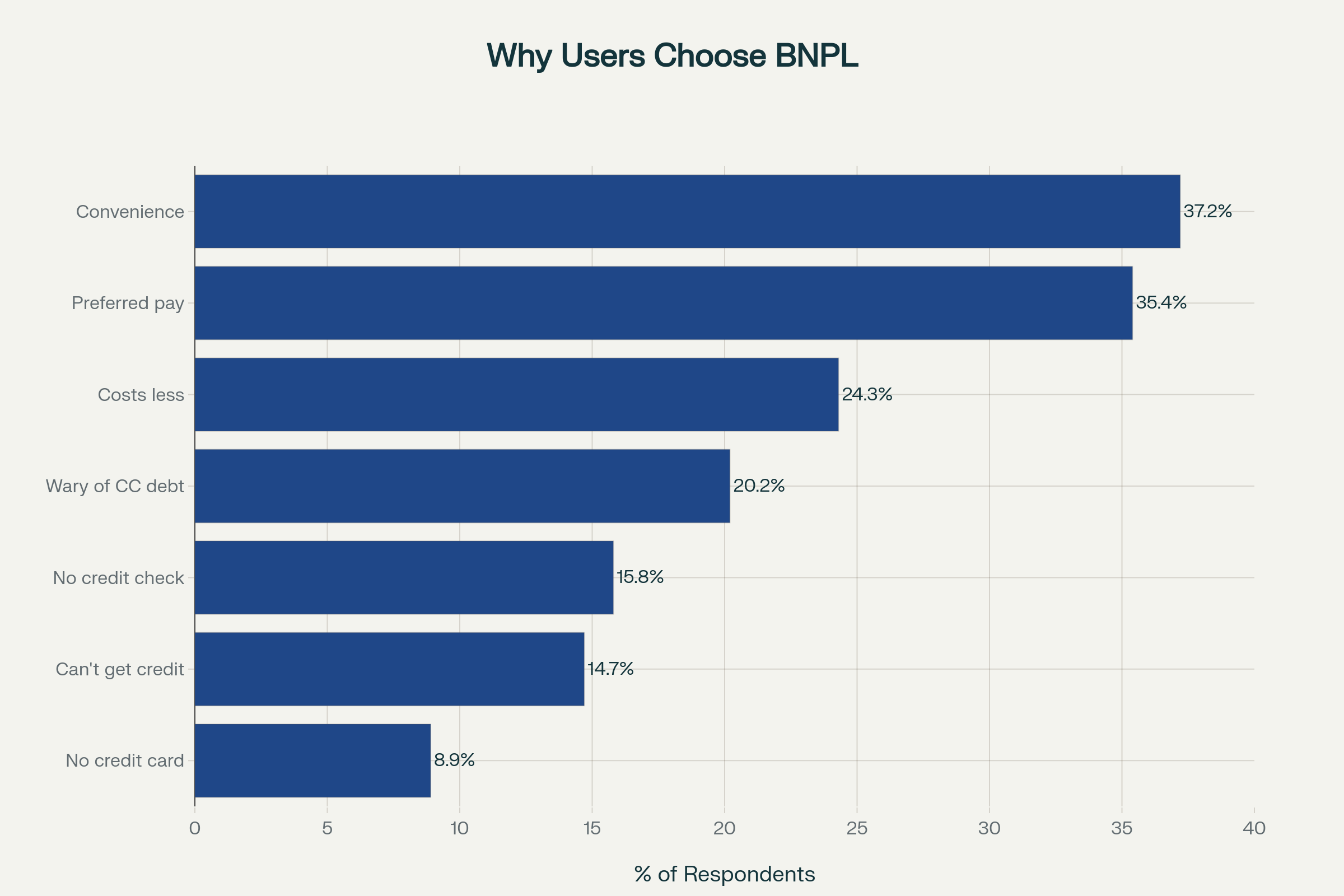

Buy Now Pay Later Statistics: Buy Now Pay Later has become one of the most influential payment innovations in today’s retail and digital commerce landscape. It is observed that BNPL has reshaped how consumers purchase products by offering flexible, interest-free installments at checkout. This shift has encouraged higher spending confidence, especially among young consumers and online shoppers who prefer quick, transparent, and short-term credit options.

Global e-commerce growth powers this shift, as platforms weave BNPL into seamless payments. Retail leads with 72.5% market share in 2025, especially fashion, electronics, and personal care, where quick approvals boost sales. Online channels dominate at 66.2%, matching mobile shopping habits, while point-of-sale options expand into physical stores.

Top Editor’s Choice

- In 2024, 86.5 million Americans used Buy Now, Pay Later services.

- U.S. shoppers spent $18.2 billion using BNPL during the 2024 holiday season.

- BNPL adoption reached 15% of U.S. adults in 2024, up from 14% in 2023.

- The average BNPL loan size is $135, showing strong use for smaller purchases.

- Most BNPL plans require a 25% down payment with 0% interest over six weeks.

- BNPL apps generated $12.5 billion in revenue in 2024, a 10.6% increase from 2023.

- Klarna earned $2.8 billion in 2024, the highest revenue among BNPL providers.

- Klarna holds an estimated 35% global market share in the BNPL sector.

- BNPL apps had 365 million global users in 2024, rising 9.2% from the previous year.

- Global BNPL app downloads reached 156 million in 2024, up by 20 million year over year.

- According to Numerator’s survey, Half of Americans have used a BNPL service according to recent surveys.

- PayPal is used by 43% of BNPL users, followed by Affirm at 37%, Klarna at 32%, and Afterpay at 30%.

- Major U.S. banks account for 27% of BNPL usage through their own programs.

- BNPL users are 75% more likely to purchase tech gadgets such as drones or robot vacuums.

- More than 41% of BNPL users reported making at least one late payment in the past year.

Buy Now Pay Later Market Size

- The global Buy Now Pay Later (BNPL) market generated USD 19.22 billion in revenue in 2024.

- The market is projected to reach USD 83.36 billion by 2034, supported by a 15.18% CAGR from 2025 to 2034.

- Asia Pacific led the market in 2024 with a 36.42% share, driven by rapid digital payments adoption.

- North America is expected to record the fastest growth, with a 15.11% CAGR during the forecast period.

- The platform/solution segment accounted for the largest share in 2024, contributing 67% of total revenue.

- Small ticket items (up to USD 300) held the biggest share at 42.98% in 2024.

- Mid-ticket items (USD 300–1000) are expected to grow at a strong 15.84% CAGR through 2034.

- The business-driven model dominated in 2024 with 70.99% market share.

- The customer-driven model is projected to expand at a 15.49% CAGR over the forecast period.

- The online segment held the leading position with 55.88% of revenue in 2024.

- The electronics sector generated the highest share at 35.94% in 2024.

- The fashion sector is anticipated to grow at a notable 15.53% CAGR during the forecast period.

(source: precedence research)

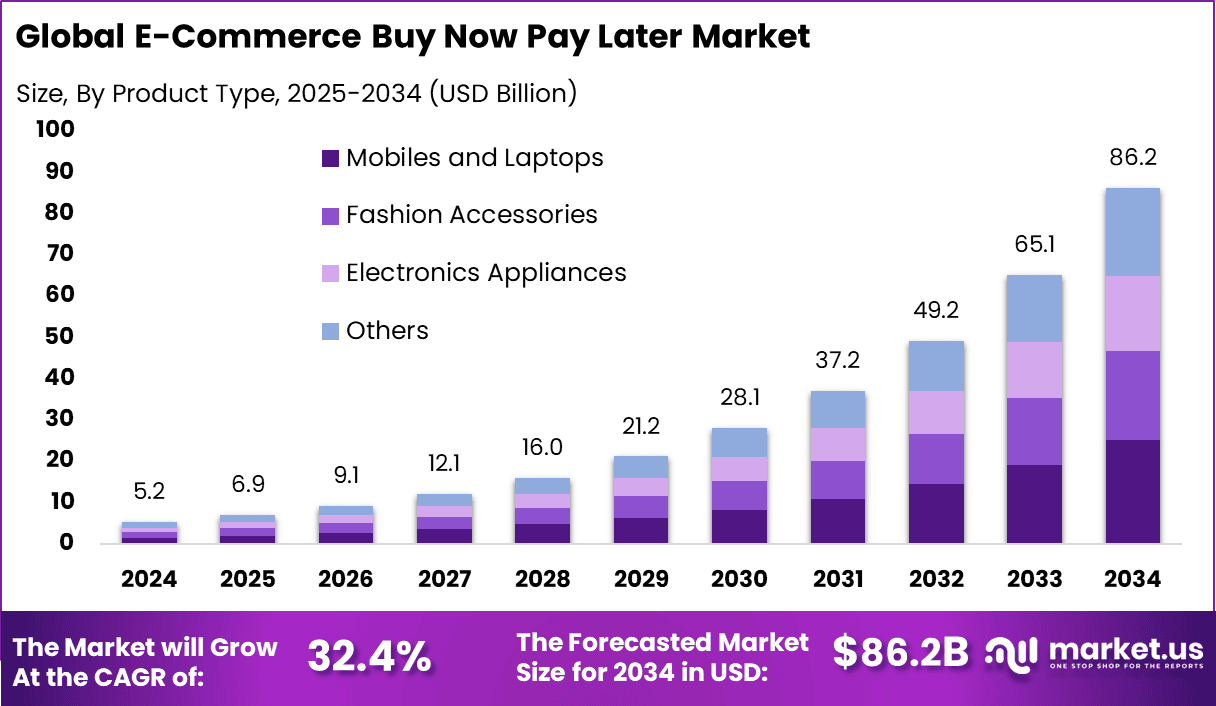

E-Commerce BNPL Market Size

- The global e-commerce market is projected to grow from USD 28.29 trillion in 2024 to USD 151.5 trillion by 2034.

- The market is set to expand at a CAGR of 18.29% during the forecast period.

- APAC led in 2024 with 45.7% share, generating USD 12.8 trillion in revenue.

- The AI in e-commerce market is forecast to rise from USD 5.79 billion in 2023 to USD 50.98 billion by 2033.

- The market will grow at a 24.3% CAGR.

- Mobiles and laptops accounted for 29.3% of total BNPL purchases, indicating strong consumer demand for high-value electronics through flexible payment options.

- Automatic repayment models represented 72.7% of usage, reflecting a clear preference for convenience and lower risk of missed payments.

- Millennials aged 26 to 40 contributed 31.2% of BNPL activity, making them the most engaged demographic in flexible payment adoption.

- North America held 34.6% of the BNPL market, supported by advanced digital payment infrastructure and high online spending patterns.

- The US market reached USD 1.62 billion with a strong CAGR of 29.3 percent, driven by rising e-commerce penetration and growing consumer demand for alternative credit solutions.

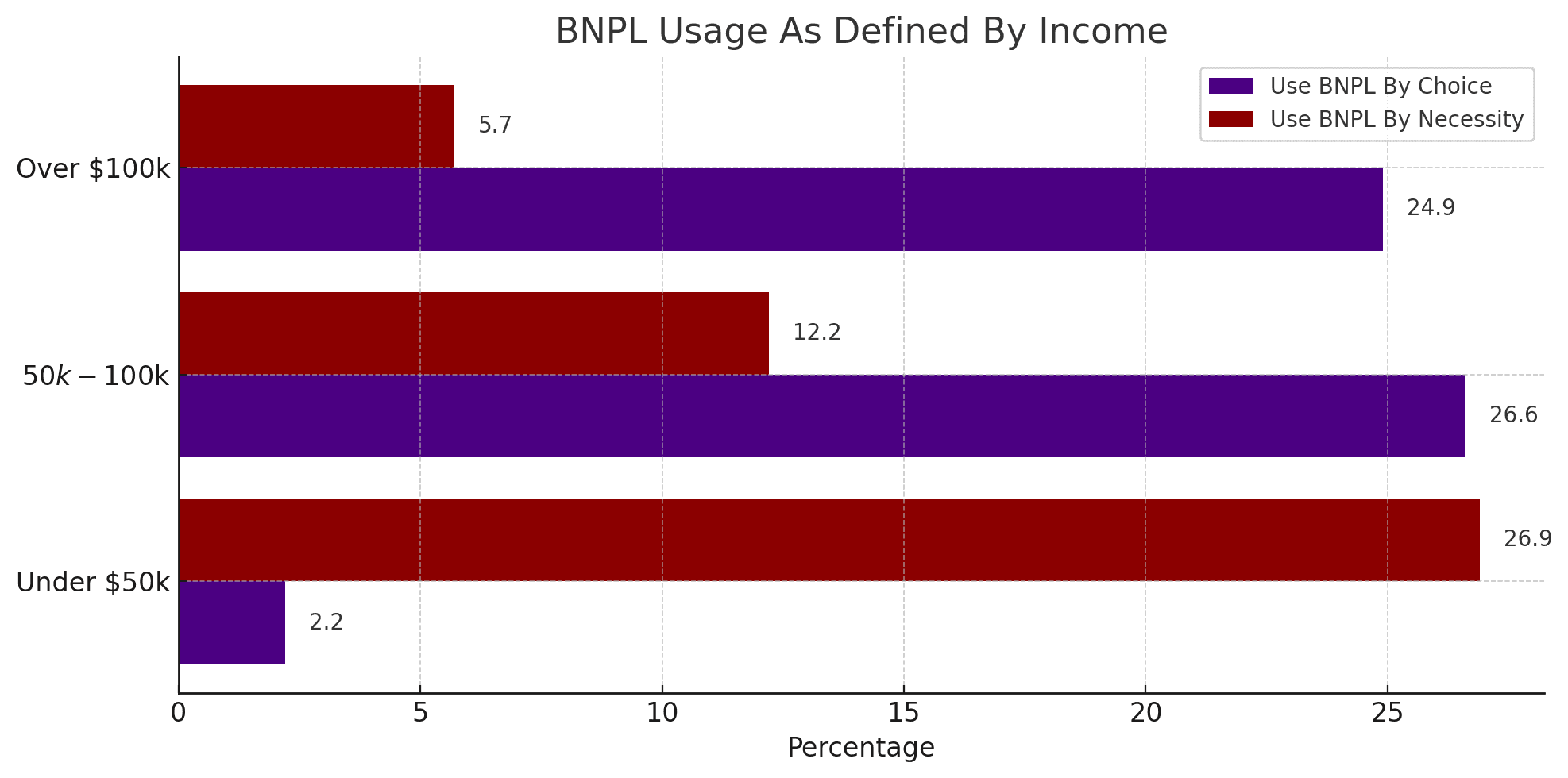

BNPL Usage by Income

(image: market.us)

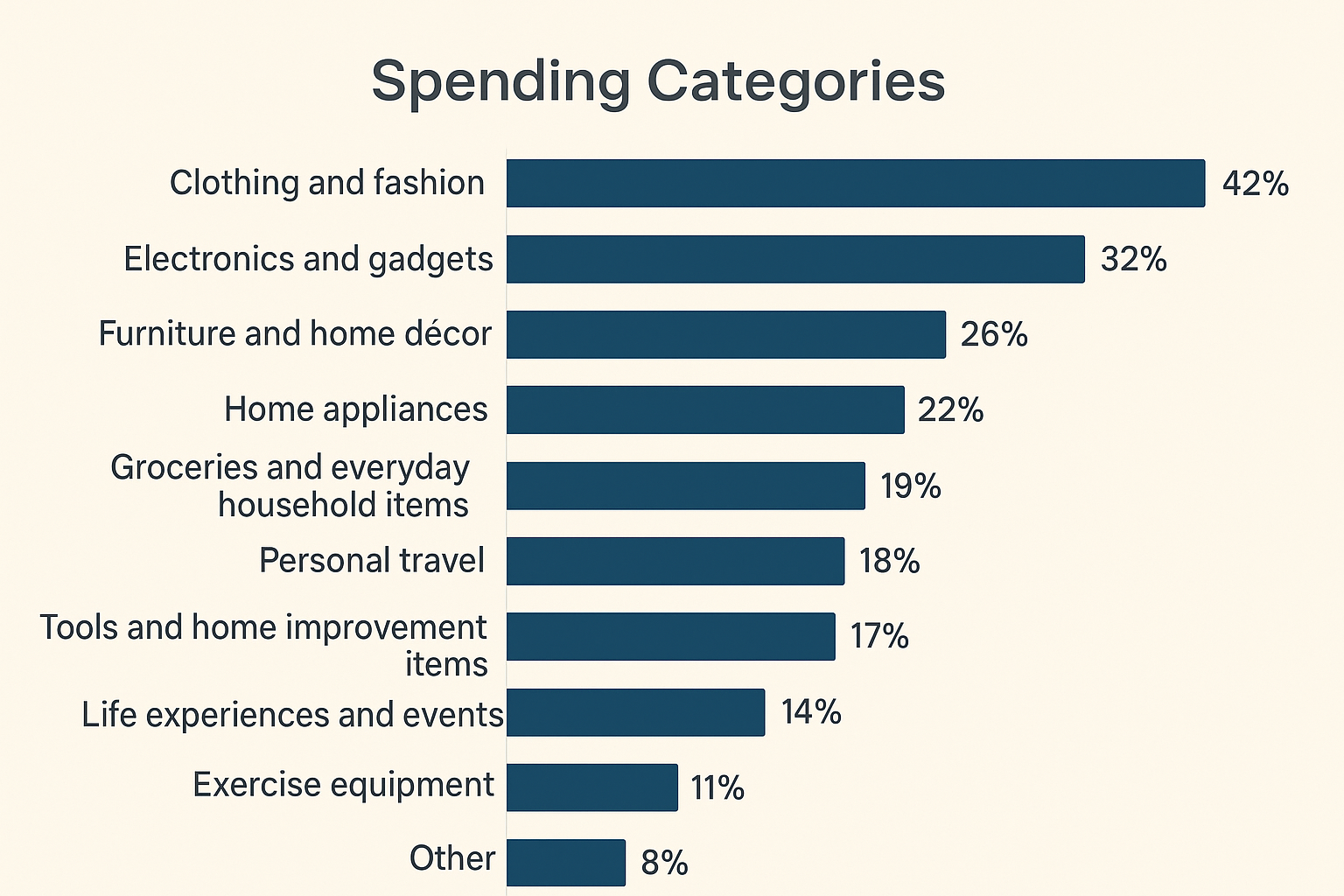

Usage by Sector

| Category | Percentage (%) |

|---|---|

| Clothing and fashion | 42% |

| Electronics and gadgets | 32% |

| Furniture and home décor | 26% |

| Home appliances | 22% |

| Groceries and everyday household items | 19% |

| Personal travel | 18% |

| Tools and home improvement items | 17% |

| Life experiences and events | 14% |

| Exercise equipment | 11% |

| Other | 8% |

(source: numerator)

BNPL Use by Age

- 48.5% of BNPL users in the United States are under 36 years old, showing that younger adults are the primary adopters of this payment method.

- 22% of consumers under 36 have borrowed using BNPL, compared with 10% of consumers over 65, indicating a strong age-based usage gap.

- Consumers younger than 36 are 54.5% more likely to use BNPL due to limited credit availability, highlighting financial access as a key driver for younger users.

- 15.6% of adults aged 40 to 60 used BNPL in the past year, representing the lowest adoption rate across age groups.

- 20.3% of consumers under 40 and 20.1% of consumers over 60 used BNPL, showing that uptake spans both younger and older demographics, although for different reasons.

- Consumers over 60 years old show the highest likelihood of using BNPL when it is offered at checkout, with 34.2% of those offered choosing this option in the past year.

| Generation | 2021 | 2023 | 2025 | % Change |

|---|---|---|---|---|

| Gen Z | 36.80% | 46.50% | 47.40% | ↑ 10.6% |

| Millennial | 30.30% | 39.50% | 40.60% | ↑ 10.3% |

| Gen X | 17.20% | 26.30% | 30.90% | ↑ 13.7% |

| Baby Boomers | 6.20% | 12% | 14.80% | ↑ 8.6% |

Use by Region insights

- In the United States, BNPL use is highest in the southern states, where 23.8% of consumers used BNPL in the past year. This rate is 35.2% higher than the national regional average.

- Among consumers in the South who were offered BNPL, 37.3% used it in the past year, showing strong responsiveness to checkout availability.

- In the West, 16.5% of consumers used BNPL, and 25.7% of those offered chose the option, indicating moderate uptake.

- In the Northeast, 15.2% of consumers used BNPL, with 21.8% of those offered adopting it, reflecting lower overall usage.

- In the Midwest, 14.8% of consumers used BNPL, and 22.8% of those offered selected it, making it the region with the lowest usage rate.

App Statistics

| Service | Percentage (%) |

|---|---|

| PayPal Credit | 57% |

| Afterpay | 29% |

| Affirm | 28% |

| Klarna | 23% |

| ZipPay | 19% |

| QuadPay | 15% |

| Uplift | 13% |

| Perpay | 11% |

| Sezzle | 8% |

| Zebit | 6% |

| Splitit | 6% |

| Other | 6% |

(reference: crresearch.com)

Risks and Regulation Insights

- Late payments and delinquency remain a major concern. Research shows that 34% to 41% of BNPL users made at least one late payment in the past year, indicating repayment difficulties for a sizable share of users.

- Debt accumulation is increasingly common. Many users hold multiple BNPL loans at the same time, often across several providers. This creates a risk of loan stacking and hidden debt that is not visible to traditional lenders or credit bureaus.

- Regulation is tightening. In May 2024, the Consumer Financial Protection Bureau (CFPB) ruled that BNPL lenders must follow consumer protection standards similar to credit card companies. This includes requirements for dispute resolution, refund processing, and clearer disclosures to improve borrower safety.

Top 7 BNPL Apps

| App | Description |

|---|---|

| Klarna | Klarna is one of the biggest buy now, pay later providers worldwide, known for its large user base and high transaction activity. |

| Affirm | Affirm is a leading BNPL service in the US, often used for bigger purchases that are paid off over longer periods. |

| Afterpay | Afterpay is the buy now, pay later service owned by Cash App, operating as Clearpay in the UK. |

| PayPal | PayPal offers a buy now, pay later option that allows users to split payments into four simple installments. |

| Sezzle | Sezzle lets users divide their purchases into four interest-free payments over six weeks. |

| Zip | Zip provides buy now, pay later options and offers a payment card that can be used for both online and in-store purchases. |

| Four | Four is a rapidly growing BNPL service in the US, offering access to premium retailers and a rewards-based experience. |

(source: business of apps)

Interesting Reads

- Embedded Finance Statistics: Market Size and Adoption

- Cybersecurity Statistics: Facts And Figures

- Digital Banking Statistics: By Market, Usage and Security Insights

Credit Cards Vs BNPL

| Aspect | Credit Cards | BNPL |

|---|---|---|

| Credit Type | Revolving line | Installment loans |

| Interest | 22.8% average APR | Often 0% if paid on time |

| Acceptance | Global, most retailers | Select partners only |

| Rewards | Cashback, points, perks | None |

| Approval | Hard credit check | Soft or no check, higher rates |

| Flexibility | Pay minimum or full, EMIs possible | Fixed schedules |

| Protections | Dispute charges, purchase protection | Limited |

Recent Developments

- In June 2025, Klarna began testing a new debit card in the U.S. through a partnership with Visa and WebBank. The card lets users pay at once or choose interest free installments for both online and in store purchases. Klarna plans to expand this card across the U.S. and Europe later in 2025 once the pilot stage is completed.

- In March 2025, DoorDash added Klarna’s Buy Now, Pay Later option to its app, giving customers the choice to pay right away, split payments into four interest free parts, or delay payment. This update is important because DoorDash holds about 63 percent of the U.S. food delivery market and follows similar moves by competitors like GrubHub.

- In May 2025, Affirm received a key regulatory approval in the UK that allows the company to operate as a lender. This approval lets Affirm offer its point of sale financing services to more merchants and consumers across the region.

Follow Us: Pinterest | X | LinkedIn | Medium

Sources:

- https://capitaloneshopping.com/research/buy-now-pay-later-statistics/

- https://www.digitalsilk.com/digital-trends/buy-now-pay-later-bnpl-statistics/

- https://www.precedenceresearch.com/buy-now-pay-later-market

- https://www.numerator.com/resources/blog/buy-now-pay-later-market-insights/

- https://www.absrbd.com/post/bnpl-statitics

- https://www.businessofapps.com/data/buy-now-pay-later-app-market/

- https://www.crresearch.com/blog/buy-now-pay-later-statistics/

- https://www.unbiased.com/discover/banking/buy-now-pay-later-statistics#What-is-the-future-of-buy-now-pay-later

- https://meetanshi.com/blog/buy-now-pay-later-statistics/

- https://explodingtopics.com/blog/bnpl-stats